Funding for the global fintech sector is at a three-year low, with venture capitalists fearing that the coronavirus pandemic will lead to a recession.

So how is that affecting fintech startups in Europe?

We've dived into regional-specific data to see exactly what's happening on our doorsteps. The health of the fintech sector can also be seen as a proxy for the wider startup scene, given financial-tech has been Europe’s largest investment category since 2013.

Here's a breakdown of the latest fintech figures in Europe*, and a view from the ground of local investors:

March saw a tangible drop in deals and volume

The graphs below provides an overview of how the coronavirus pandemic has impacted the number of fintech deals and the amount raised, with March recording a noticeable drop.

Overall, March was the lowest month for fintech funding in three years, with the exception of November 2019 and December 2018.

As shown on the right graph, March saw €338m in fintech funding, while February saw more than double that, with €825m (including Revolut's $500m raise).

The funding drop in March could be treated as an anomaly, but a far larger drop is now expected to follow. Indeed, the severity was not fully felt in Europe until half-way into March. Moreover, most recent deals were likely already in the late stages when the pandemic struck, granting founders some leverage. Some younger funds are also now reportedly struggling to do draw-downs from their limited partners, as fears worsen.

That suggests a "dry spell" is lurking, according to nearly a dozen industry sources consulted by Sifted.

"If you’re a founder and need to raise external money in the three months, plus you're also seeing 40% downturn in [business] activity — you’re absolutely terrified," says Tim Levene from Augmentum, a fintech-focused venture capital fund.

Nonetheless, he argues fintech may be better insulated than other sectors from a capital retreat, given it's attracted investors with deep pockets and long-term ambitions.

Better clarity should come in the coming month, he adds, as we get new data and concrete political decisions. One figure to look out for in late-June is how much European fintechs raised across the first two quarters of 2020 (last year, the sector raised $5.1bn in the first six months). So far, it's raised $2bn per Dealroom data, with much of that concentrated in January and February.

The UK is still on top for fintech

A geographical analysis of the funding data also shows the UK's continued dominance in terms of deal numbers last month.

This seems to have continued into the first month of Q2, with April seeing a flourish of big deals in the UK. Among the stand-out raises recorded so far this month are online ID-checker Onfido, business-to-business fintech Previse and open-banking platforms Railsbank and Yapily, as reported by Sifted.

For now then, the UK is holding onto its crown as Europe's fintech capital (Britain made up 50% of total European investment flows in fintech last year).

Nonetheless, Germany has also seen a strong start to April. Trading app Trade Republic reportedly closed a €50m round last week and Taxfix confirmed a similarly large round. Both startups were listed in Sifted's list of fastest-growing German fintechs earlier this year.

Who's fundraising?

There are several large fintechs currently on the fundraising trail, including Monzo, Monese, Habito and Sweden's Dreams.

A spokesperson for Curve also confirmed the company was in early talks for another fundraising round to fuel growth.

Several fintechs who raised their Series A over a year ago are also due for more funding. That includes the likes of financial-wellness app Cleo, rental-app Canopy, Farewill (which does online wills) and open-banking company Bud.

Elsewhere, a survey of 277 anonymous, UK finance-based startups revealed that over 50% have less than six months in cash left and need funding soon. Those who can afford to will likely wait until they're on better footing.

While it won't be an easy ride as revenues slump, founders could point to the added need for online financial tools amid the lockdown.

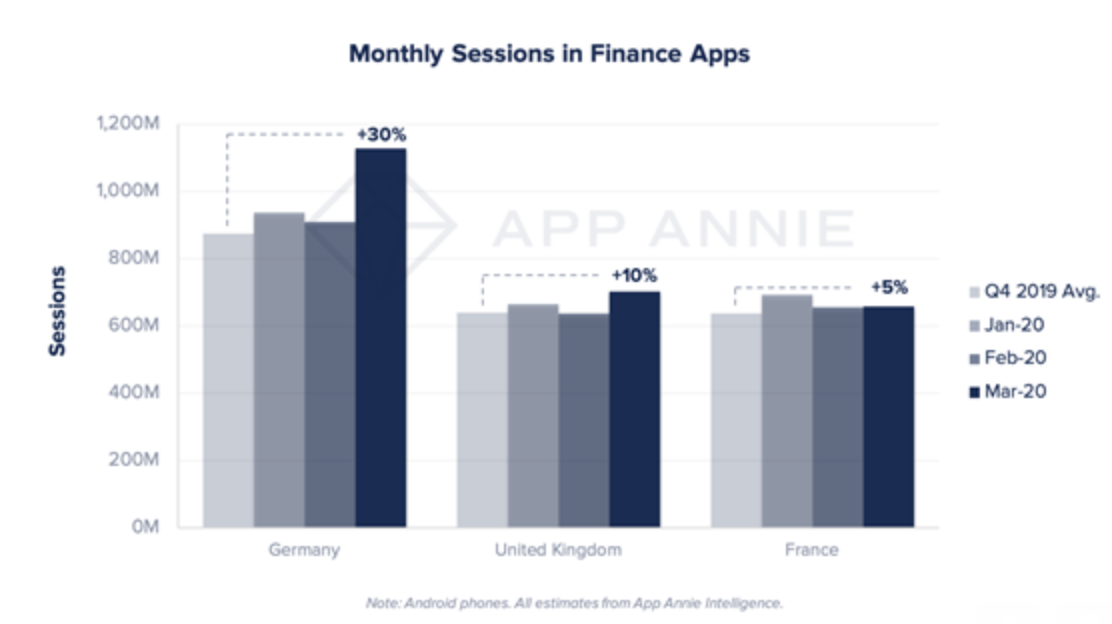

Insights from mobile data aggregator App Annie shows that usage of consumer-finance apps were up by 30% last month in Germany, compared to Q4. There's also been a small boost for digital financial tools in France and the UK, with activity concentrated in apps like Klarna, PayPal and French money-transfer tool Lydia.

Still, the underlying uncertainty means those that secure funding at this time are getting a clear vote of confidence — even if they're forced to adjust their valuations.

Who's still investing and where?

Despite the disruption facing fintechs, venture capitalists are taking a long-term view — telling Sifted they still see fintech as a wildly attractive sector.

For instance, Anthemis, a London-based fintech specialist fund, has closed two seed rounds in the past weeks. Both are yet to be announced but are expected to be in the insuretech sector.

Another London VC, Albion, led Credit Kudos' £5m at the beginning of the month and said another fintech Series A was set to be announced this week.

Meanwhile, Europe's most active fintech VC — Sweden's NFT — seem more bullish than ever. Lead partner Johan Lundberg said the fund's portfolio looks better than expected.

“I thought we’d be in a bad situation but I’ve been happily surprised.”

He added: “I think fintech will be one of the most successful industries of this crisis, along with home delivery and groceries. It should be one of the winners here.” Still, it's worth noting that Swedish fintechs may be performing better given the country's more relaxed approach to lockdown.

- Read more: Who's funding European fintechs?

Elsewhere, Finch Capital are scouting out trading and digital mortgage-brokers startups, predicting these sub-sectors will surge in the post-coronavirus world.

Element Ventures, a business-to-business fintech VC, is also heavy on the look-out, with ongoing talks happening around six or seven new deals.

"We're genuinely open to business," partner Michael McFadgen told Sifted. "We're a really early fund so we have both the time and the capital to put in... We're trying not to be too skittish about this."

Later-stage companies can also really on their early investors to drive 'inside rounds', with many VCs solely doubling down on their previous investments.

DN Capital and Augmentum both said they were focusing on their current portfolios and largely closed-off to new ventures.

Meanwhile, Index Ventures closed two large fintech rounds with Taxfix and Alan this month, having backed the latter before.

*A note on the data

For clarity, this data is taken from Dealroom and encapsulates banking and payments, insuretech and proptech.

It relies completely on companies self-reporting their fundraises, meaning there are plenty of deals that go unannounced. Not everyone will be logging their raises publicly — particularly 'inside rounds' like top-ups — meaning the actual drop in funding may be less severe than that recorded in March.

"When closing a funding round, founders usually ask themselves when’s the best time to announce it? And “immediately” may not be the right answer... Aligning the announcement timeline, with a product launch or a recruiting campaign is usually the way to go," French VC BlackFin noted in a blog post.

"We may be experiencing some shyness around deal announcements."

Having said that, seed-stage companies are less prone to concealing their raises than Series A and Series B companies. This means it's more likely the funding volumes are under-recorded, as opposed to the number of deals (given seed rounds are the most common).