With their savvy interfaces, smart features and oodles of VC money, digital banks have become the poster-child for fintech.

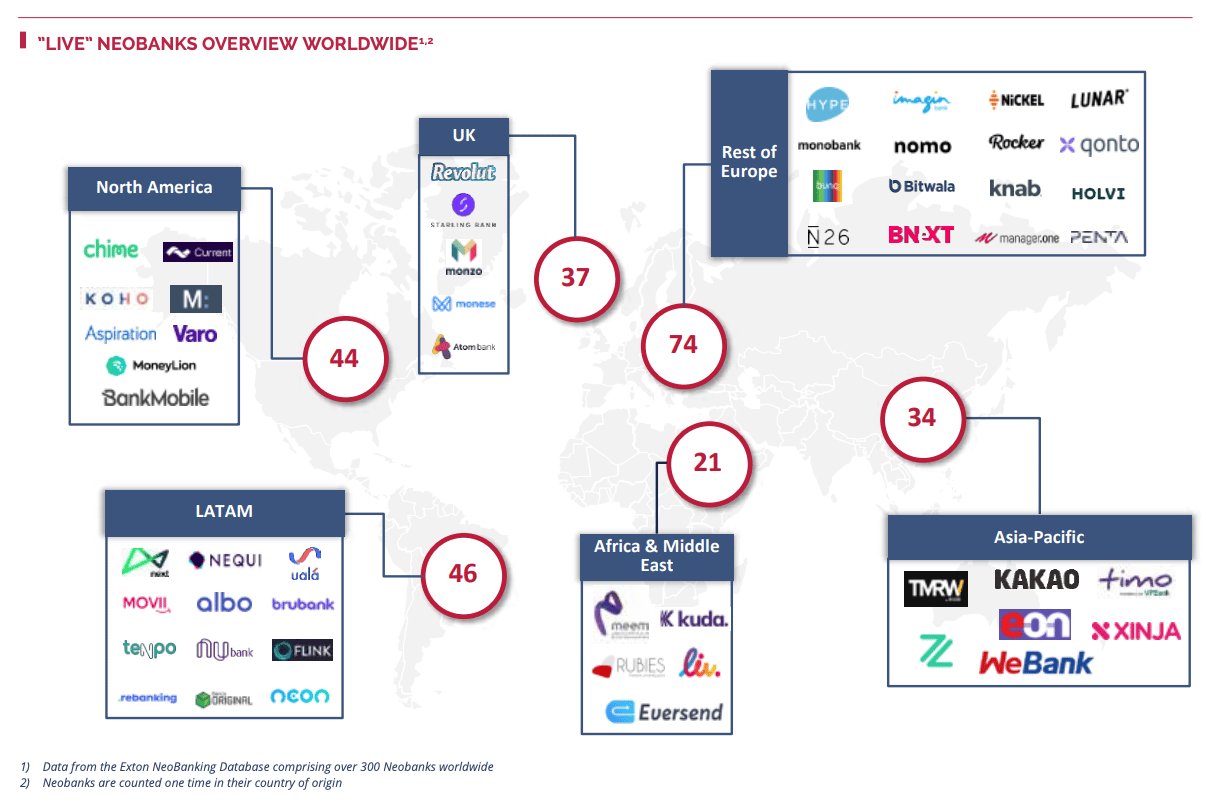

There are now almost 300 so-called "neobanks" live worldwide, with nearly half concentrated in Europe.

Meanwhile, new players are continuing to join the ranks, particularly in Latin America, Africa and the Middle East. This boom is being fuelled by ongoing investor enthusiasm for the sector, with neobanks raising over $2bn in venture capital globally this year alone.

Customers are also riding the neobank wave. PitchBook estimates that by 2024, 145m of us will be using these apps across North America and Europe alone.

To help keep track of the global neobank landscape, we have broken down the key data and trends.

For clarity, 'neobank' is defined here as an app that i) offers its own retail banking services (i.e. prepaid, debit, credit cards), ii) launched after 2010, and iii) is mobile-centric.* This definition does not distinguish between regulatory status, but it's worth noting that only a handful have official bank licences.

Here is the story of the world's neobanks, as told in numbers.

The neobank boom: At its peak?

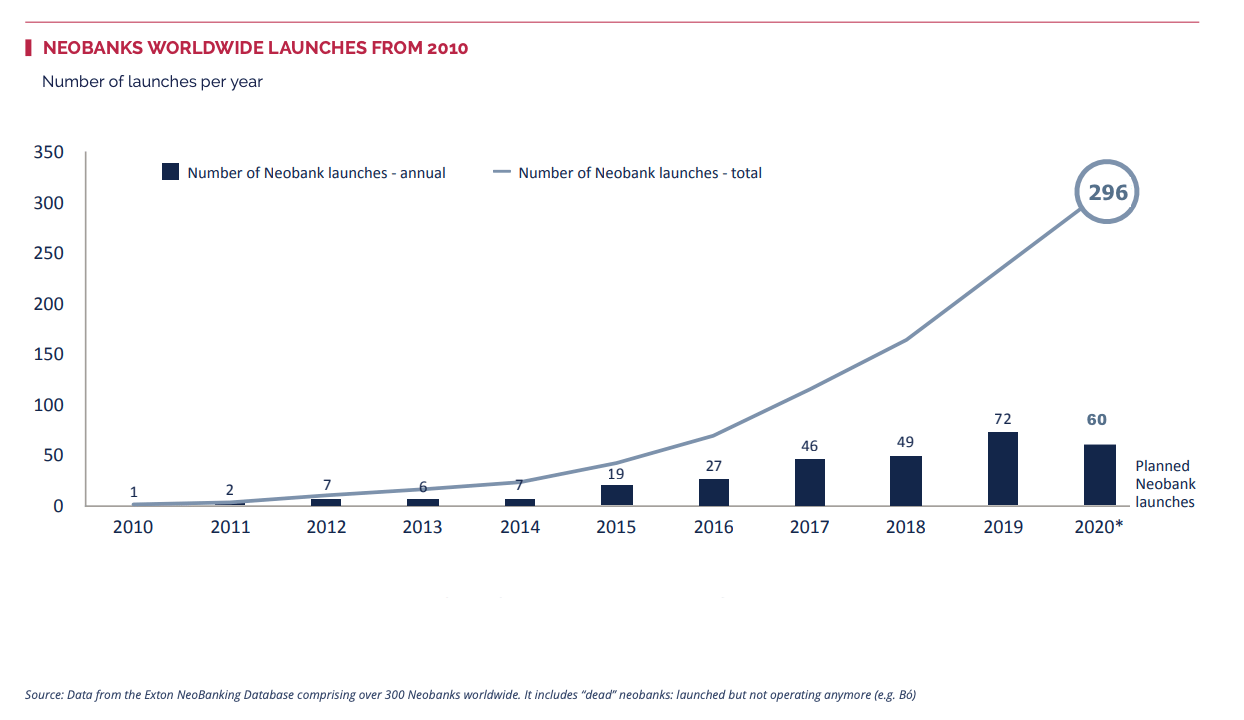

The number of neobanks worldwide has tripled since 2017, climbing from 100 to nearly 300 worldwide.

That means, over the last three years, a neobank launched every five days somewhere in the world (!), according to Exton, a consultancy firm which manages a global database of consumer banking apps.

In 2019 alone, more than 70 neobanks went live globally.

But Cristoph Stegmeier, a partner at Exton, says we may finally have reached a peak, with 2020 seeing a slowdown.

"I expect we will see less from now," he told Sifted.

He explained this year's launch decline went beyond simply the 'Covid effect' and stems from the growing saturation of neobanks. Indeed, 30 neobanks have been wound down since 2015, according to Stegmeier.

Still, the neobank boom hasn't totally stalled.

Over 30 neobanks launched in the face of the pandemic, including Zelf, Daylight (a US bank for LGBT+ members) and Tenpo in Chile.

Meanwhile, dozens of new players are still planning to go live in 2021 — including Greece's Woli and France's Vybe.

Geographical hot spots

Europe spawned the first wave of neobanks, and now counts over 100 live apps and 50m accounts, according to Exton's database.

Within this, the UK is a particular hotspot, having produced 37 neobanks (making up one-third of Europe's total). It is now the world's most active neobank market, courtesy of its head start in the space and its strong digital infrastructure.

"Europe is still the engine for [neobank] innovation," Exton told Sifted, with Sweden and France joining the UK among the world's top five most active neobank markets.

The world's largest neobanks

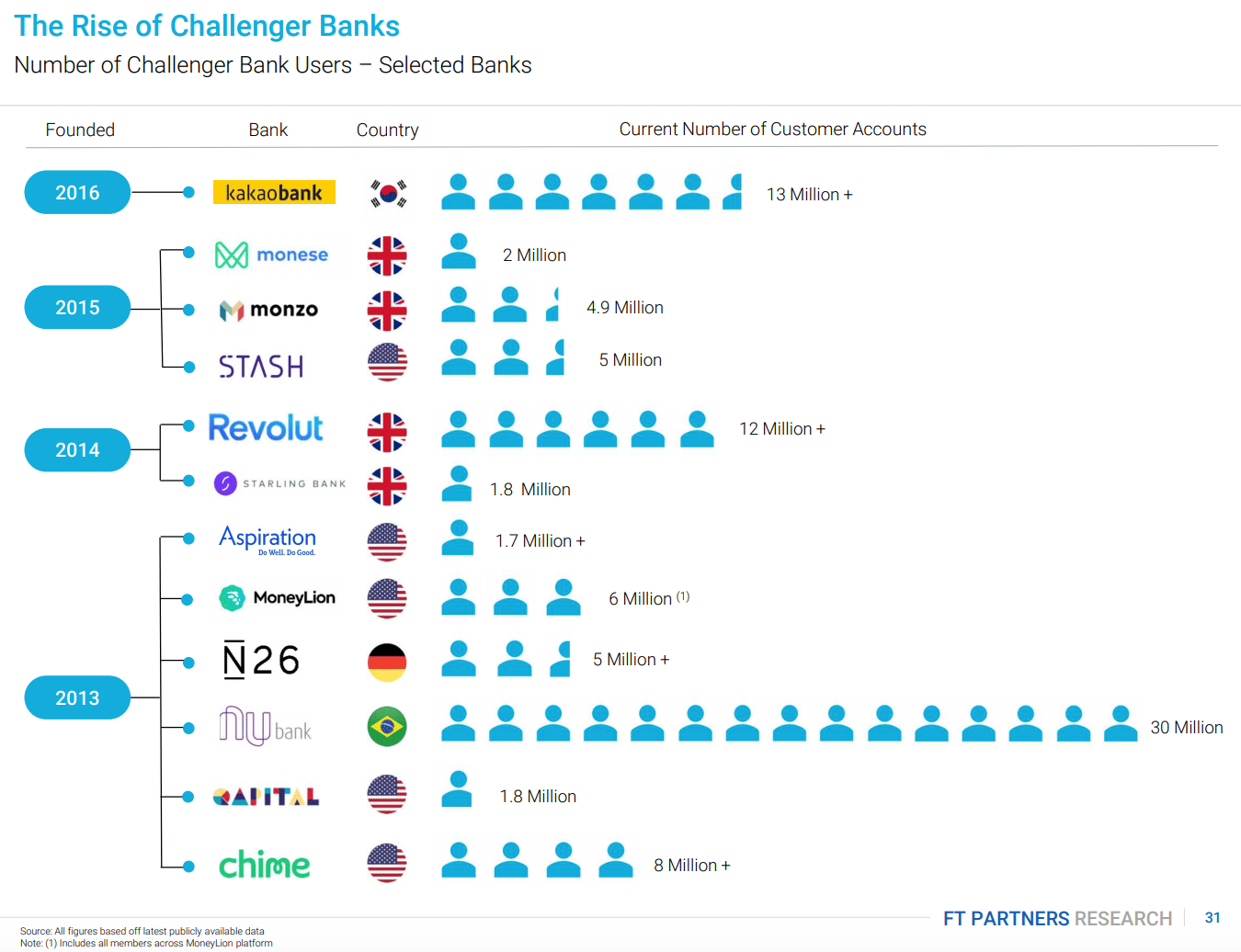

There may be hundreds of neobanks, but a small handful lead the pack.

US-based Chime tops the global valuation list with a price-tag of $14.5bn, while Brazil's Nubank tops the leaderboard for the most customers, claiming to have 30m users.

Notably, most leading neobanks have built up audiences exclusively in their home markets.

Currently, just 43 of the world's neobanks (~17%) work across multiple geographies. Competing on multiple fronts is no easy feat, and several neobanks have been forced to retreat — with N26 and Holvi withdrawing from the UK. This is partly due to the complexities of passporting financial services and licensing.

One exception to this rule however is Revolut, which has expanded to 30+ markets to date and currently leads in Europe by app downloads.

Still, the neobank leaderboard is still very much open to disruption, says Exton's Stegmeier.

"Existing large neobanks won’t be the ones to stay on top if they miss out on emerging opportunities,” he told Sifted, adding he has been "disappointed" by the lack of innovation among the top players.

The incumbent surge

The world's neobanks are run by an eclectic group of people. Students, seasoned entrepreneurs, consultants, engineers and veteran bankers are all behind some of the world's top neobanks.

But it's not just startups launching neobanks.

Legacy banks are also entering the fray, with the likes of Standard Chartered launching Mox and RBS bringing Mettle to the SME market.

In fact, 27% of today's neobanks are offshoots of traditional banks, according to Exton's database.

These are known as the "greenfield" approach — whereby traditional banks spin out standalone digital apps, built on a separate infrastructure, and suggests banks are slowly waking up to the need for digitisation.

Meanwhile, 'independent' (or startup) neobanks also face the threat of 'consumer fintechs' increasingly morphing into banking players. For instance, TransferWise is a foreign exchange platform but now offers a travel card, while buy-now-pay-later providers like Klarna now offer full spending cards in some geographies.

So far, 16% of the 300 live neobanks have been spun out of existing consumer fintechs.

Covid-19 hit some neobanks hard

The pandemic has been a challenging year for fintech — including for neobanks.

The lockdown exposed digital banks' reliance on interchange fees and travel for revenue.

Covid even claimed several neobank casualties, including the UK's Tandem — which pivoted away from consumer credit cards, having once been ranked among the top 10 global players — and Australia's Xinja.

On the flip side, mobile-first apps became the obvious destination for customers unable to access bank branches... at least in some cases.

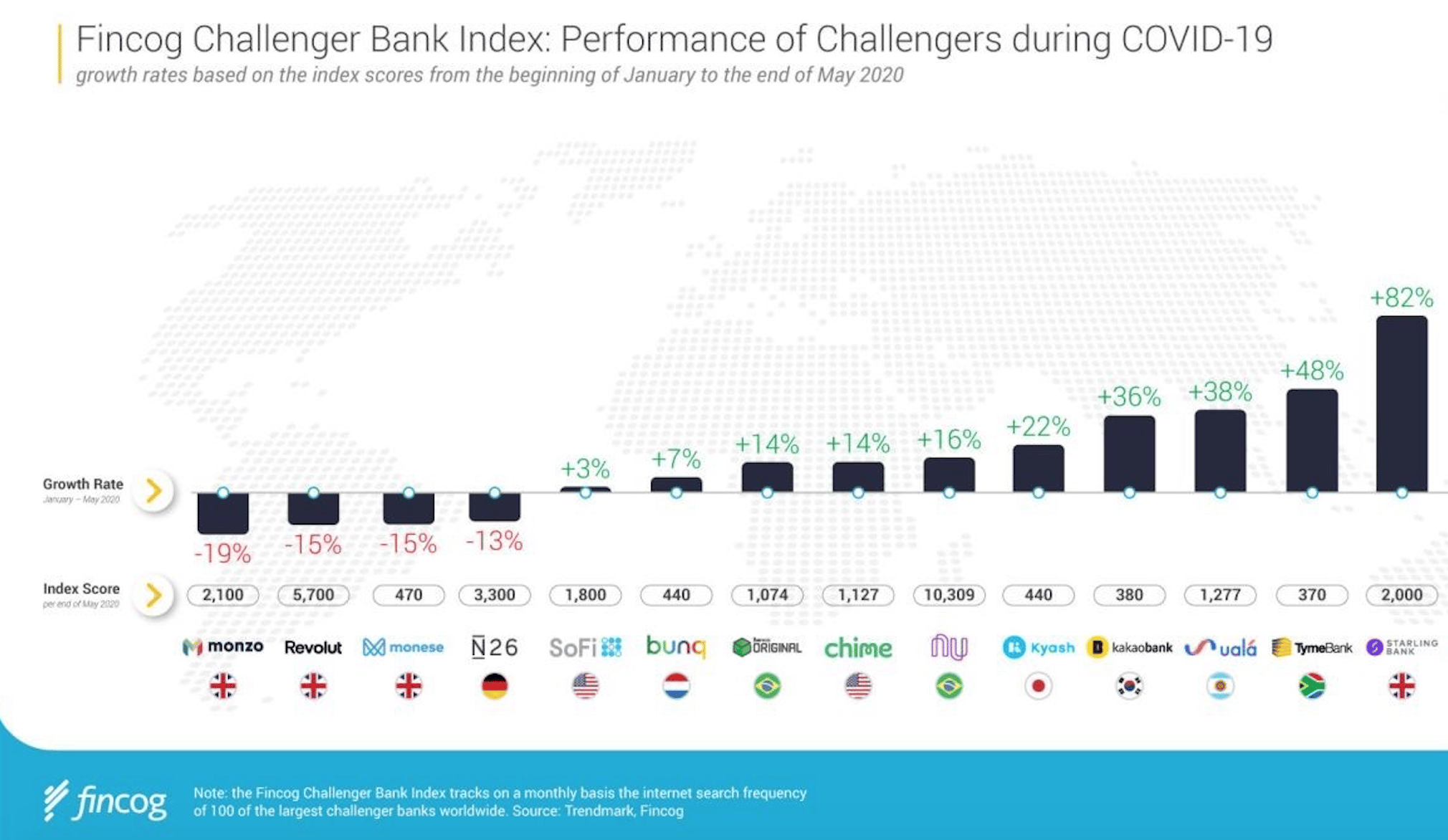

The graph below shows the impact of Covid on different neobanks, using the change in internet-search frequency between January and May as a proxy.

According to this data, European digital banks stalled the most during lockdown.

One key variable is that Europe's neobanks were excluded from distributing government loan schemes. For instance, N26 was unable to process unemployment payments in Spain, while French and German SME neobanks could not distribute government funds. Meanwhile, UK neobanks were eventually included in the schemes, but some complained it took too long.

Neobank trends to watch in 2021

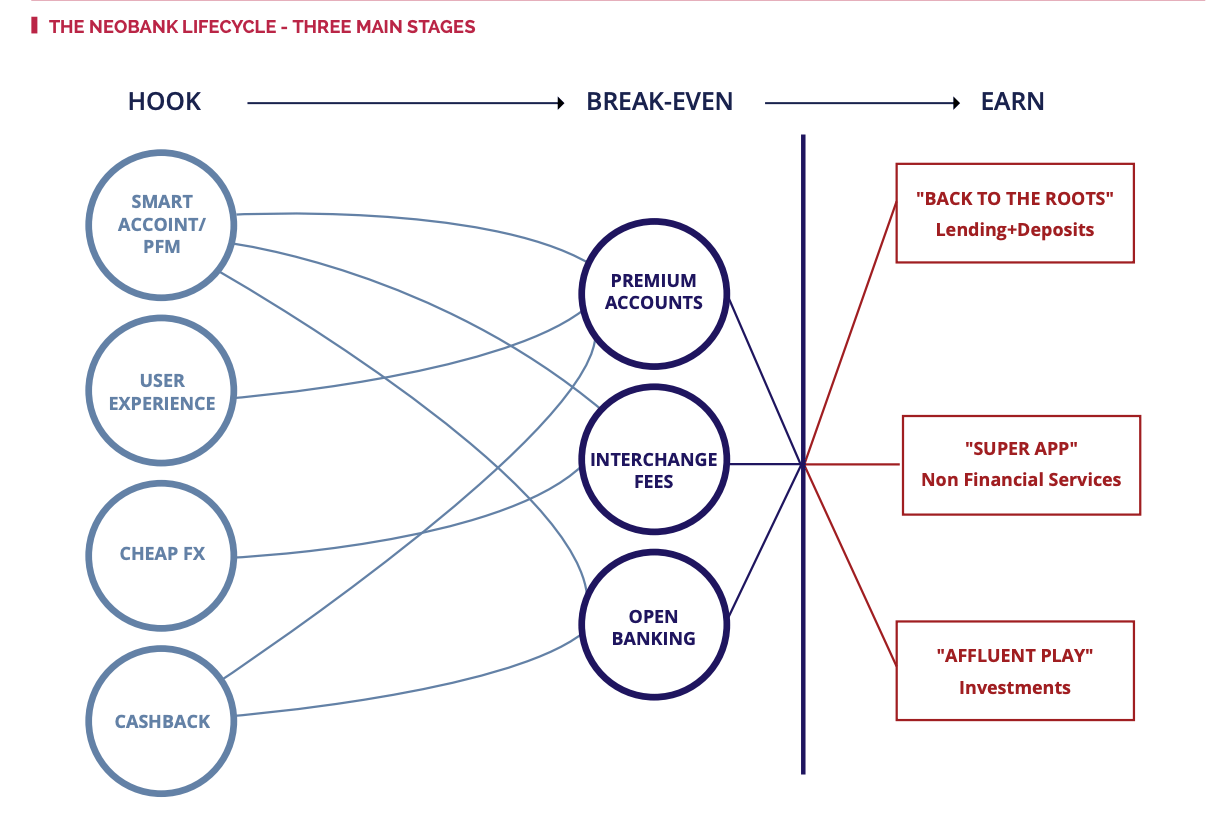

Broadly speaking, neobanks make money in three ways: payment transaction fees, premium subscriptions, and commissions from third party services.

But this hasn't proven a smooth model for profitability.

Some of the larger players are now experimenting with launching B2B products. For instance, Starling is developing a Banking-as-a-service proposition, while Revolut is building a payments gateway.

The neobank business model may therefore adopt the following evolution:

To this end, the following trends could well shape 2021's neobanking landscape:

- The rise of smaller, niche newcomers, moving away from the "growth at all costs" norm

- Strengthening regulatory / compliance teams

- Refocus on core products & geographies, prompting retreat from highly competitive spaces

- Focus on hiring local leadership teams

- Adoption of “new” revenue sources

- Increased lending efforts, boosted by careful credit risk management

- Pivot from official bank licences to third party regulation

- Heightened regulatory scrutiny

* By Exton's definition, a neobank must also prioritise "new products and new technology, with a focus on transparency and innovation, aiming for a primary customer relationship – not just solving a particular process or product pain point."