In 1987, Europe played host to the largest ever R&D project on driverless vehicles. The Prometheus Project pulled in €749m in funding from the intergovernmental organisation Eureka — which included 20 European countries like the UK, France, and Germany at the time — and was supported by dozens of car makers as well as academic institutions.

Its mandate was to look into the use of tech like AI to develop autonomous vehicles (AVs) and a safer road traffic system, and it culminated in a self-driving car making the 1,000-mile journey from Munich to Copenhagen and back in 1995.

Nearly 30 years — and many billions of investor dollars — later you could be forgiven for wondering where all the AVs on the roads are. Slow-to-update legislation, public mistrust and technological limitations have all hampered the sector’s growth.

But recent developments in AI are ushering in a “revolution” for AVs, says Paul Newman, cofounder and CTO at UK-based Oxa, which is building software for self-driving vehicles. “If you look at the methods we were using five years ago — it’s not clear that we would have [eventually developed fully self-driving vehicles].”

Now — because of the rise of generative AI and “enormous neural networks with billions of parameters” — “it’s an inevitability”.

Buoyed by VC confidence and increasingly favourable regulation, European AV companies are making strides towards taking their driverless vehicles to the roads. But one big question remains: how do you commercialise a technology that’s still a work in progress?

The AI ‘step change’

Over the past few years, there have been a growing number of examples of AVs driving on public roads across the globe.

In the US, for example — where regulation is further along than in Europe — companies like Alphabet-backed Waymo and General Motors’ Cruise have launched self-driving taxis. In China, AVs have driven a similar number of kilometres on the roads — 70m as of September 2023, according to data from management consulting company Bain. Things have moved slower in Europe, but AVs have made it onto some roads in France and Germany and there have been several autonomous vehicle pilots and trials in the UK.

Those vehicles have reached what’s known as level 4 autonomy — where a vehicle can perform all tasks in set circumstances, in a specific, geofenced location.

But the holy grail of autonomous driving — level 5 autonomy, which means a vehicle can perform all driving tasks in an environment under any conditions — has eluded AV companies.

AVs tend to use a combination of cameras, radar and lidar (a method for working out distances by measuring the time it takes for light to reflect off an object from a laser) to take in their surroundings and make decisions on how to behave. The key to building truly AVs that can drive anywhere is training the AI to make the right decisions when faced with an infinite amount of unlikely but possible scenarios on the roads.

With GenAI, that’s becoming a more realistic prospect. Previously, AVs would need to be specifically programmed with scenarios. But the foundational models that underpin AI have become so good at coming up with them on their own that that’s no longer the case, says Newman.

“GenAI is proving very useful in enabling us to virtually drive many more miles in many more environments and with many more challenges,” he tells Sifted. “For example, you can drive a street once but it [didn’t used to] properly train the AI to deal with the scene in all circumstances — flood water might cover road markings, fog could obscure other infrastructure and people may step out unexpectedly.”

But, using GenAI, Oxa can train its AI in a “metaverse” which takes a single driving environment and replicates it in many different conditions. The technology has led to a “step change” in how AVs can be trained, says Newman. “We don’t need to drive around to find the weird cases anymore.”

This “self-supervised learning” has been made possible by the “incredible transformation” in the ability of AI to generalise [applying knowledge to new scenarios] and adapt to new environments over the past few years, says Erez Dagan, president at Wayve — a UK-based company developing software for AVs.

“AI's generalisation power gives us the ability to build safer AV systems that can adapt to new cities, new vehicle types and rare situations that the AI model may not have been trained on,” he says.

AI models have also got better at ‘explaining’ why they’ve made decisions — something that’s seen as key to building public trust in AVs.

Earlier this week, Wayve announced it’s developed a new model that helps explain and determine driving behaviour combining a vision model, which makes sense of what the model sees, and a language model, which was traditionally used to predict the next words in sentences.

According to the company, it’s the first time a vision-language-action model (VLAM) — which is seen as a promising area of research in AI robotics — has been tested on public roads.

VC confidence

The promise of breakneck advances in what’s possible with AI has seen VCs' confidence in the European AV sector remain high through the downturn.

Last year, AV startups in Europe raised $969m, according to Dealroom, just shy of the record $1.1bn they picked up in 2022. Over that same period, funding into European tech overall dropped by a third.

Much of that funding has come from several large rounds. In September last year, UK-based Conigital, which provides AV solutions for industrial use, raised a £400m Series A; in January Oxa picked up $140m. In 2022, both Wayve and Sweden's Einride, which is developing AV tech for freight mobility, picked up $200m rounds.

Another reason for investor optimism about the European AV sector is that regulation in the region is progressing. In the UK, an AV bill is being pushed through parliament, which could see self-driving cars on the roads by 2026. Germany and France already allow autonomous vehicles up to level four on their roads in certain areas, and the EU also has regulation that sets out specific requirements for autonomous vehicles coming into force this year.

There’s also Europe’s track record in automotive manufacturing. Four of the 10 biggest car makers in the world are based here — and every one of those companies is working on autonomous driving solutions.

It presents a big commercial opportunity for European startups building the software and hardware that can power AVs, says Seth Winterroth, partner at US VC Eclipse, which has backed Wayve.

“The current state of play for many [automotive manufacturers] looking at an AV future is deciding whether to build or buy,” he tells Sifted. “Today, we’re increasingly seeing [automotive manufacturers] who have bought into these solutions.”

Where’s the money?

But it’s still early days in the sector and right now, most AV companies are in the initial stages of commercial deployment.

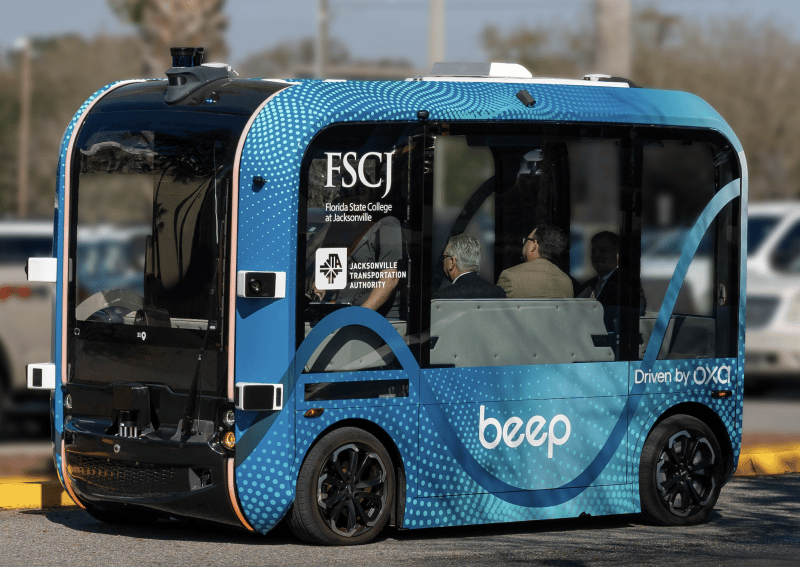

Oxa, which is focusing on building software for AV uses in passenger shuttles and industrial logistics, launched its first commercial deployment — shuttling passengers around Florida — in February this year. The startup says it will launch seven more passenger services in US and UK cities in 2024.

Wayve doesn’t have any revenue-generating deals announced yet. In the near term, the startup is looking to work with car makers which are keen to add automated driving features to their vehicles. “Longer-term, we'll see autonomous mobility solutions like fully automated robotaxis and delivery fleets,” says Dagan.

But pressure to make money is starting to ramp up.

“The AV sector is facing a crossroad where it is crucial to showcase the business case of deploying autonomous,” says Henrik Green, general manager of autonomous technologies at Einride. “While the technology for autonomy is getting closer, the real challenge lies in aligning business models to support widespread adoption.”

Einride has turned to what it calls “incremental automation” in its hunt for revenue. It has deployed autonomy in its trucks bit by bit as regulation and technology permits — rather than waiting until it has a fully autonomous vehicle to release a commercial product.

As part of a commercial project with US-based GE Appliances focused on implementing electric and autonomous delivery fleets to the company’s supply chain that began in 2021, Einride completed a public road pilot of its autonomous truck in 2022. A year later, the company says that a level of autonomous driving had become part of day-to-day operations.

“As time goes by, we aim to increase the autonomous part as the technology matures and regulation catches up,” Einride cofounder and CEO Robert Falck told Sifted last year.

Germany’s Fernride, which is building AV solutions for private, industrial yards, has focused on that area because regulatory barriers are fewer than on public roads — something it hopes will mean it can commercialise quicker.

“Everyone [in the AV industry] was so frustrated with progress in the past 10 years and nobody has been able to deploy a commercial product,” founder and CEO Hendrik Kramer told Sifted when Fernride raised a $31m Series A last year. “We wanted to tackle a use case that we could deploy now, and buy ourselves some time to win the trust of customers and build a viable business.”

That approach is paying out. Fernride raised a €17.8m Series A extension in September last year and Kramer says the startup has since signed contracts worth “double-digit millions”.

But right now, no European AV companies are commercialising at scale, and alongside solving the enormous technical challenge of developing a vehicle that can drive itself on a road it’s never seen before, it’s one of the biggest challenges facing the sector. And it’s one those companies are all too aware of.

“For every AV company in Europe (and the world), there is a big sense of urgency to start generating revenues,” says Kramer. “In the next couple of years, we will see that there will be winners and losers in the industry.”