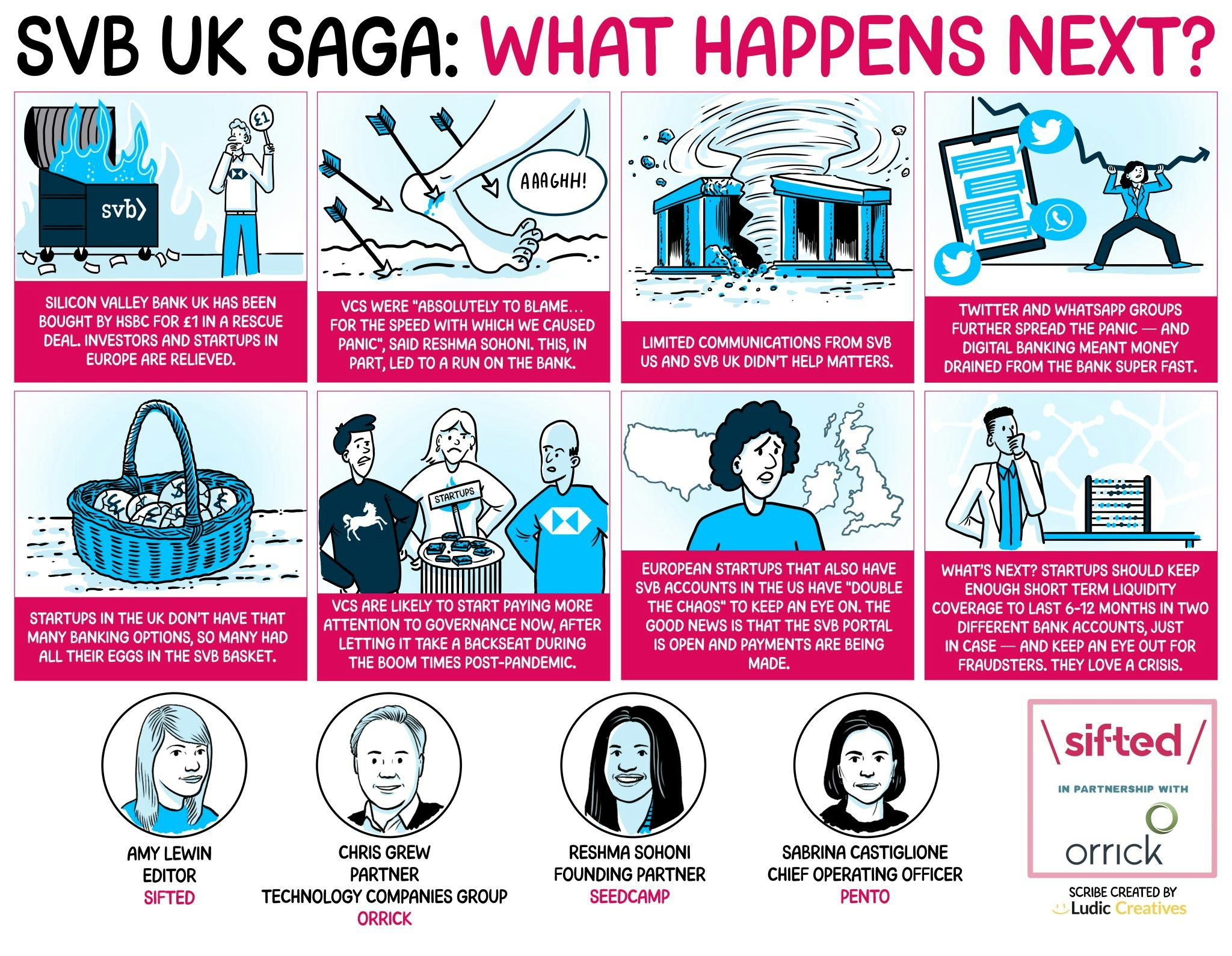

As founders and VCs alike finally get some rest after the chaos of Silicon Valley Bank’s collapse — and dramatic rescue by HSBC in the UK — many are starting to reflect on what the hell happened, what happens next and what we can all learn from it.

And fingers are pointing at some people more than others: VCs.

Were VCs responsible for the chaos?

In a Sifted Talks on Tuesday, Reshma Sohoni, founding partner of early-stage investor Seedcamp, said that VCs were “absolutely to blame as a collective industry for the speed with which we caused panic”.

By Friday, VCs all over Europe and the US had emailed portfolio companies encouraging them to diversify their cash holdings and move money out of SVB accounts. Some VCs had also asked their investors not to wire capital to SVB. WhatsApp groups and tweets repeated the message.

Seedcamp didn’t take that view. Its European portfolio, says Sohoni, didn’t look too exposed — and many of the startups that did bank with SVB UK had their money in 30-day notice (or longer) accounts, so wouldn’t have been able to get it out anyway.

Every VC firm had to look after its own assets and had “fiduciary duties to protect their companies

A bank run — which is ultimately what occurred — would be bad news for them. "You can’t choose one child over another,” she said.

Chris Grew, a partner in the technology companies group at law firm Orrick, said the finger shouldn’t be solely pointed at VCs. While the bank run was “unfortunate”, he said, ultimately every VC firm had to look after its own assets and had “fiduciary duties to protect their companies”.

Why did startups have so much money in just one bank?

There are some particularities to the tech ecosystem which didn’t help matters.

Pento COO Sabrina Castiglione said some (extremely unlucky) startups that had literally just raised a funding round found themselves with a whole lot of capital in one SVB account.

1,300 UK startups, Grew noted, also had SVB as their sole bank — a move he described as “poor money management”.

But, as Sohoni pointed out, there are good reasons why startups centralised money in SVB. Opening accounts with traditional banks can often require companies to have historical records, which early-stage startups don’t have. High street bank accounts can also take longer to open due to additional checks for these risky-seeming and unprofitable businesses; an unwelcome delay when startups have VCs ready to wire them capital.

SVB, on the other hand, “understood their customers”; they’d ask about factors like runway, ARR or pitch decks when startups applied for accounts, not profitability.

SVB — and its people — would be missed by the ecosystem if the buyout had fallen through, said Grew.

Do startups need to prepare better for ‘black swan’ events?

The take-away from all this isn’t that startups should prepare for a whole host of "black swan" events that could hit them, said Castiglione and Sohoni.

Your biggest competitive advantage isn’t the size of exposure or cash in the bank — it’s how fast you can move

Castiglione said that when running a startup “safely at a low cost”, the priority isn’t to save as many pounds as possible; it’s to save as many minutes as possible. “The most valuable commodity hasn’t been money, it’s been time.”

Startups need to be able to easily allocate money to sales and marketing activities to grow their customer base, and to research and development. “Your biggest competitive advantage isn’t the size of exposure or cash in the bank — it’s how fast you can move,” said Castiglione.

But VCs do need to start paying more attention to “hygiene” factors like money management, said Sohoni. The weekend has proven, she said, that “governance has taken a back seat” in the past few years of high competition, super speedy growth and funding frenzies. Grew said the onus is on startups to appoint someone to make those fiduciary decisions, regardless of size.

Castiglione questioned how feasible it is for startups to vet how sound their bank is on an ongoing basis — especially when a tiny early-stage company won’t have the resources or skills needed.

What practical actions can startups take now?

Startups that bank with SVB US should set up another account as soon as possible, and redirect money that will otherwise head to their SVB US accounts, as the future of the US bank remains unclear.

Startups should also look out for scams. “Fraudsters love a crisis,” warned Castiglione, adding that anyone with control of money needs to be on “high alert,” especially if they fit the profile of a company that would bank with SVB.

Bigger companies should ramp up their checks with encrypted portals, multi-factor authentication and ID verification, she said. Smaller teams without those resources should verify every new payee’s identity via video call, and set up a two-tick system to approve any interactions involving money.

Founders should also diversify where they hold their money: this crisis could happen to any bank, so keep enough short term liquidity coverage to last six to twelve months in two different accounts, just in case.

And remember, Castiglione said, money in SVB UK is now relatively secure. Rather than move money between accounts, instead focus on the money coming into and going out of any startup.

And, finally, what should VCs and government be thinking about?

“Panic is the worst, we need to all manage that and be more thoughtful of the action we should take in any crisis situation,” said Sohoni. “And we need to continue the conversations around when should government step in, what kind of policies need to be put in place to encourage speed and innovation — but with enough safety margin.”

Missed the event? Watch the full Sifted Talks here: