Challenger banks like Monzo may have no immediate plans to sell-up, but their fellow European fintech startups have shown there's money out there waiting for them.

The sale of European fintechs via initial public offerings or acquisitions has pulled in €83bn over the past six years, according to a new report by Dealroom.co and Finch Capital. This is twice as much as the next biggest category, enterprise software, and highlights the scale of opportunity for investors as well as the growing maturity of the fintech market.

Some of the biggest exits were the €7.1bn flotation of Dutch payments company Adyen and the sale of Swedish start-up iZettle to Paypal for $2.2bn last year.

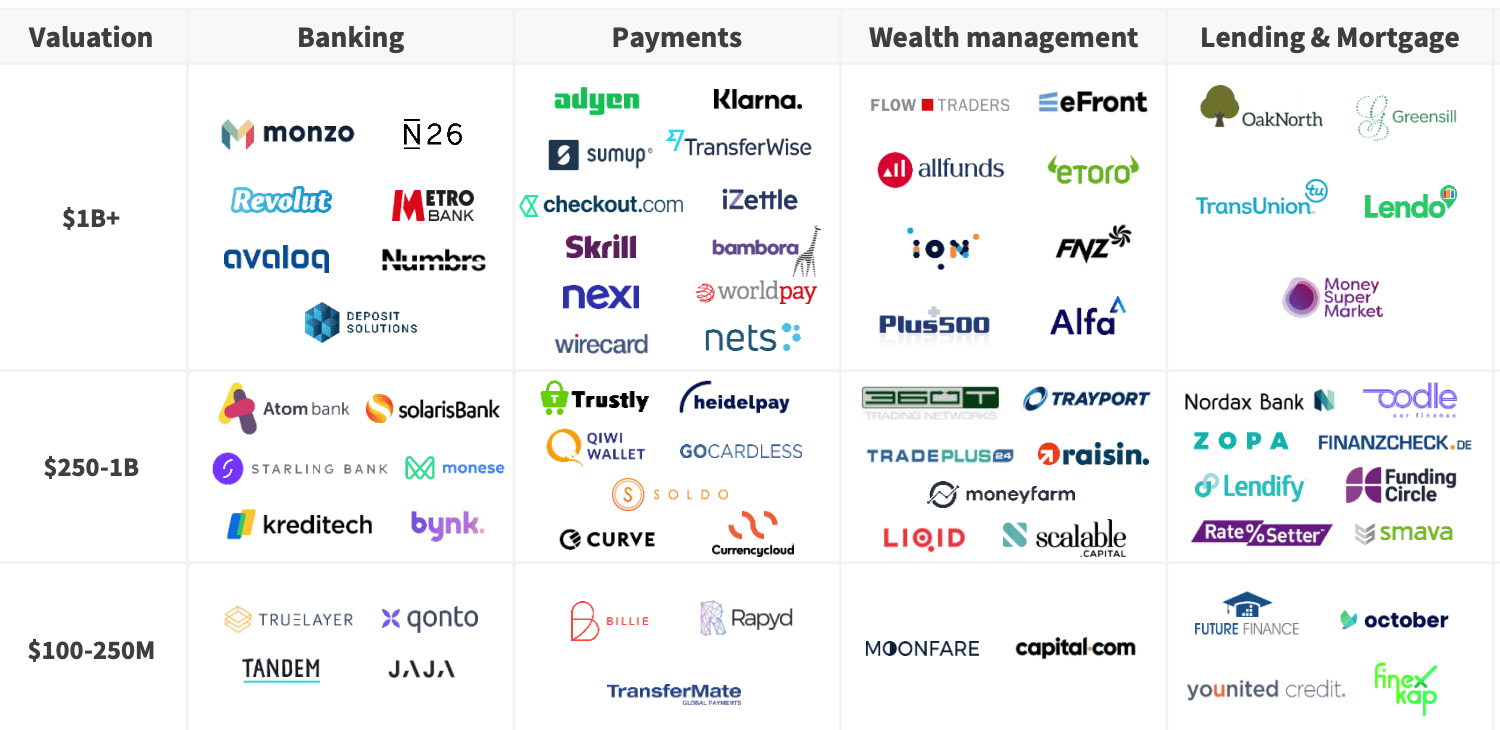

The same report also estimates that the continent's remaining private fintechs have an "unrealised" value of €43bn combined, including companies such as N26 and Starling Bank.

For clarity, the report methodology includes four groups under the broad "fintech" umbrella; banking & payments, insurtech, proptech and firms enabling fintech (encompassing blockchain and artificial intelligence developers).

Venture Capital frenzy

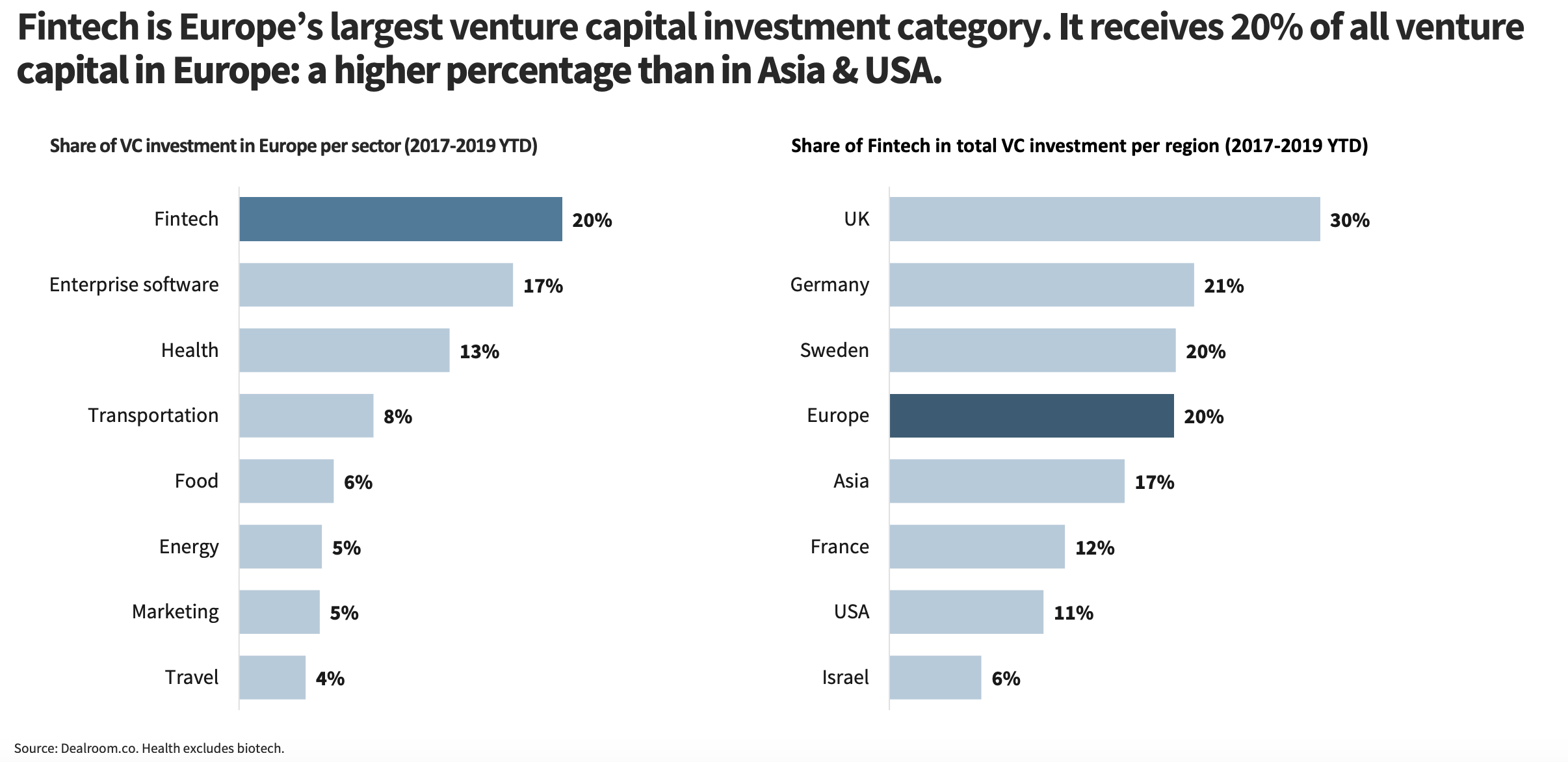

One of the trends underpinning fintechs' exit-surge is the huge (and growing) venture capital buzz in the space. Since 2013, fintech has been Europe’s largest investment category, receiving 20% of all venture capital into the region: a higher percentage than in Asia and the US.

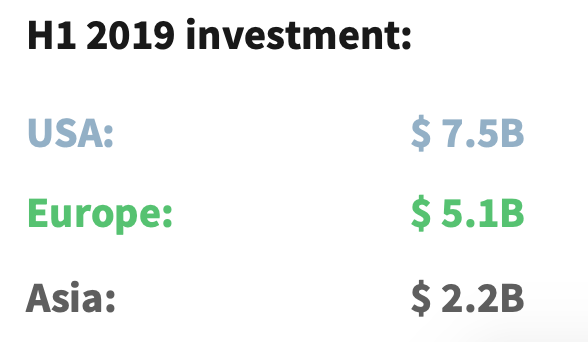

Notably, the total amount of fintech funding in Europe overtook Asia for the first time in Q1 2019, when capital in the East plummeted. If the current trajectories continue, Europe could also catch up with the US.

It's worth noting that the UK has the highest percentage of fintech investment globally, with 30% of its total venture capital funding directed towards fintechs. That trend is set to continue into 2020 as local challenger Revolut eyes a $1.5bn raise, according to reports, while WeSwap and FreeTrade, an investment app, both eye sizeable Series B, Sifted has learned.

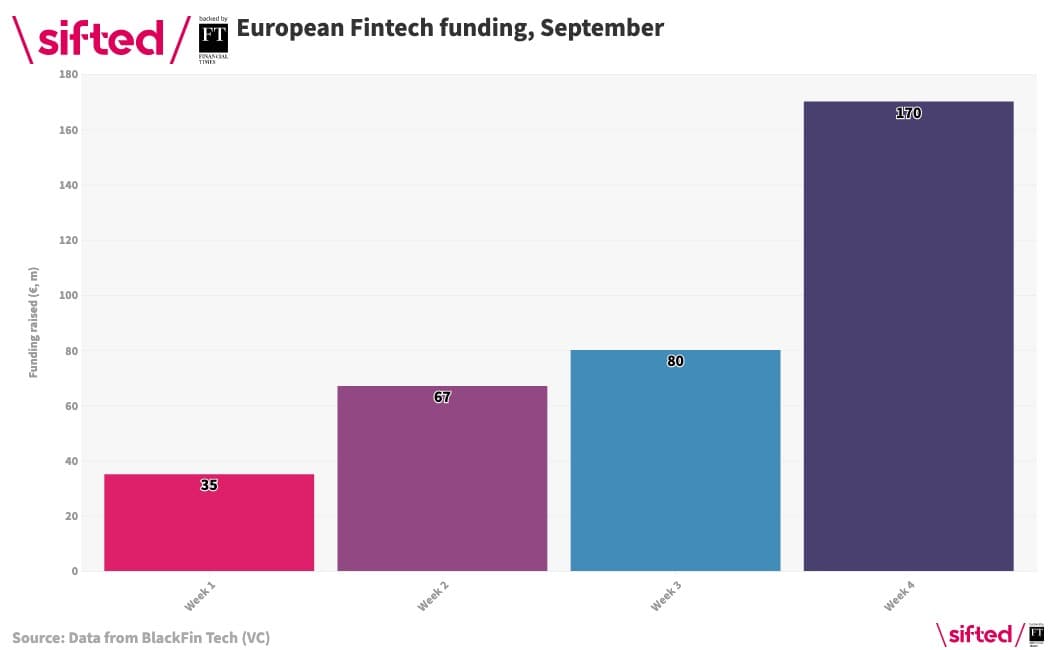

To give a snapshot, European fintech funding raised around €352m last month alone, largely concentrated in €10m+ rounds and primarily led by local venture capitalists. Meanwhile, the challenger banks have raised €2.4bn already this year, led by N26's July raise.

Equally, the rise in fintech funding has not been in isolation. Overall investment in startups reached new records in 2019, and in Q3 alone, European startups (including fintechs) brought in €8.7bn of venture capital funds.

Top fintech exits

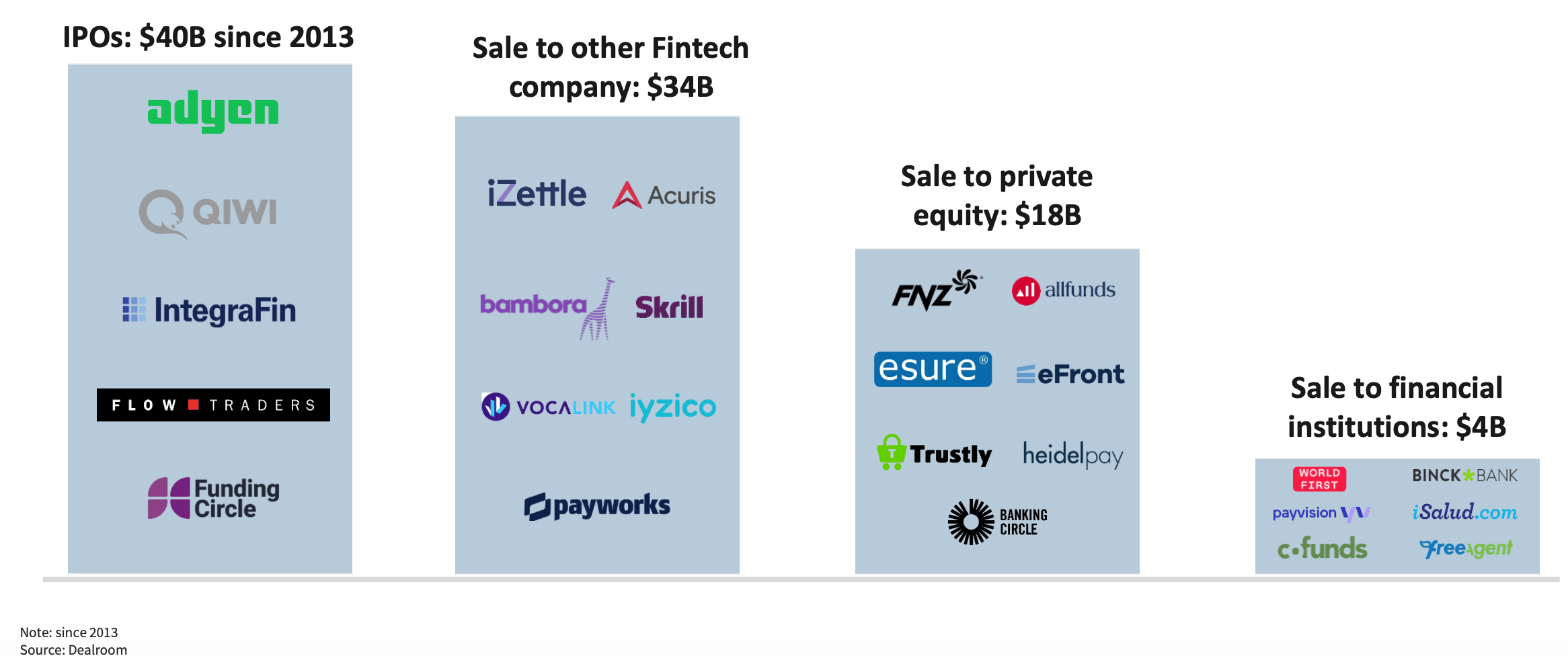

The most viable paths to exit have been via an initial public offering ($40bn), sale to other fintechs ($34bn), and sales to private equity firm ($18bn).

The final column shows how traditional banks have been relatively absent from big fintech acquisitions, although Goldman Sachs has been a major late-stage financier in Raisin and Nutmeg.

Top trends

The report also flagged the following key areas:

- Central and Eastern Europe (CEE) is seeing a growth in digital payments, which new businesses are tapping in to.

- In addition to SME loans and consumer loans, challenger lenders are now focusing on mortgages.

- Most wealth management apps are using algorithms or fully automated-management to aid investment decisions.

- Banks focused on SMEs are increasingly targeting startups & gig economy workers.

- While Europe has rising stars across nearly every fintech key vertical (from banking & payments to insurance and enabled software), there are few that individually cut across multiple verticals. In other words, they operate in silos; a trend criticised by a McKinsey partner.

Fintech overview

Week-by-week September fintech funding