It looked to be the perfect end to a successful year for WeSwap, the travel money-swap startup, which last December hoped to win not only the prestige of going public on the London markets but also a cool £20m in new funding.

But at the last minute, the company got spooked.

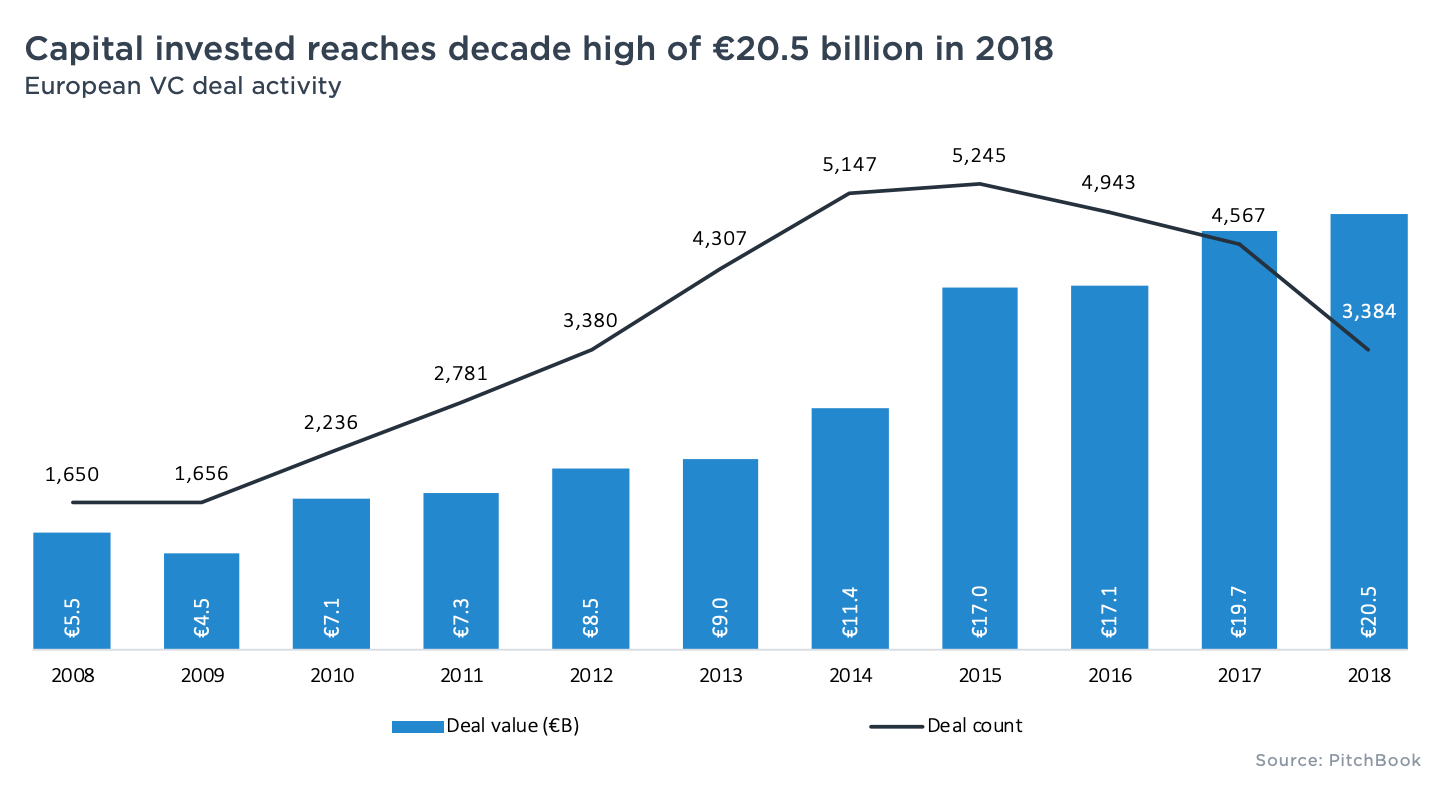

First, they watched peer-to-peer lender Funding Circle — the UK’s first major fintech listing — sink on the public market, with shares dropping 24% below the target price at one point.

We no longer had the capital we thought we’d have to grow, so we had to switch plan.

Then, the wider UK stock tanked. In the days leading up to WeSwap’s planned listing, the FTSE 100 started to wobble, with shares down around 6% through the month.

Not the ideal backdrop for WeSwap, whose listing was always going to be small and risky.

“That’s the crazy thing about IPOs for [loss making, high-risk] companies like ours. It’s dependent entirely on how the market is feeling that day. Just that one day,” chief executive Jared Jesner tells Sifted.

“It became impossible to do it at a sensible valuation.”

So on a foggy winter morning last year — the day before the listing was scheduled — Jesner pulled the plug. Months of roadshows and heavy-duty accounting efforts scrapped. Hopes of making it into the fintech history books fizzled.

“We no longer had the capital we thought we’d have to grow, so we had to switch plan. We focused on bringing costs down,” Jesner recalls.

Specifically, the company is now on track to have slashed 40% in costs over a year. That includes cutting its workforce by 20%; in particular, developers who had been hired to oversee the scaling plans post-listing.

An unexpected growth spurt

Fortunately for WeSwap, the overhaul does not seem to have done long-term harm. Jesner says the company’s revenues have grown by 30% since December, stemming from increased user acquisition as a result of 15 large partnerships, including travel booking-site Skyscanner.

The company makes nearly all its money through margins on its currency swaps, offering the inter-bank rate plus a 1% or 2% fee to load up pre-paid FX cards. The company recently announced it had traded £250m in global currencies since launching in 2015, translating to millions in revenue. WeSwap also capitalises on its wealth of travel-data, securing targeted partnerships in key travel destinations.

WeSwap expects to break even in 20 months

Indeed, WeSwap expects to break even in 20 months, with one last substantial raise planned for early 2020.

Challenging the challenger banks?

Jesner, a likeable Scotsman, targets people he understands; savvy travel-lovers aged 35-50, tired of the bureau de change’s crippling rates yet suspicious of digital banks.

Indeed, he's stood firm against VC advice that WeSwap should become another Revolut, and apparently convinced them that older groups prefer buying temporary cards to switching banks.

“Prior to this year, investors were like ‘be a digital bank’, but now fintech is starting to settle down,” Jesner says.

Jesner's business case is that challenger banks do not currently appeal to WeSwap’s older audience and that WeSwap can offer equally — if not more — competitive currency-swap rates. However, if full-service digital banks begin to draw in the older generation, however, WeSwap could be in trouble.

Jesner's thesis also doesn't solve the issue of money-transfer service Transferwise, which also now has its own travel card. While it charges per transaction at a fluctuating rate rather than in one lump sum, it has the advantage of having raised $773m; WeSwap has raised ~$30m. Transferwise also offers twice as many currency swaps.

Next stop: Emerging markets

All too aware of the encroaching competition, Jesner is on the innovation-war path again, buoyed by another £2.3m crowdfunding effort this summer.

Perhaps most importantly, WeSwap is set to launch in India this December, hoping to charge 50% more in fees than in the UK. The major target will be middle-class travellers and students heading abroad. And Jesner hints India will be the first of many emerging markets they look to conquer once they've tackled the regulatory obstacles.

WeSwap is also focused on introducing more diverse products and revenue streams next year, introducing instantaneous flight-delay insurance, AI-based savings assistance, and travel-lending.

“We’re not just about FX. We’re going to be a complete travel companion."

So bar the uncertainty around Brexit, Jesner is now quietly confident about the future. And while he’s shelved the IPO prospect for the near future, there are still no regrets.

“Building your own company, having to innovate everyday…it’s the adventure of a lifetime."