If you haven't heard of Pipe yet, it's about time you did. The US fintech was valued at $2bn last week, reaching unicorn status less than a year after launch.

Pitched as one of the buzziest new finance startups around, Pipe helps companies who charge subscriptions get some of that recurring revenue upfront. So instead of raising fresh funding from VCs or taking a loan, companies can get 'advances' on fixed revenue.

But a flurry of European startups have started mimicking Pipe's model, to local investors' delight.

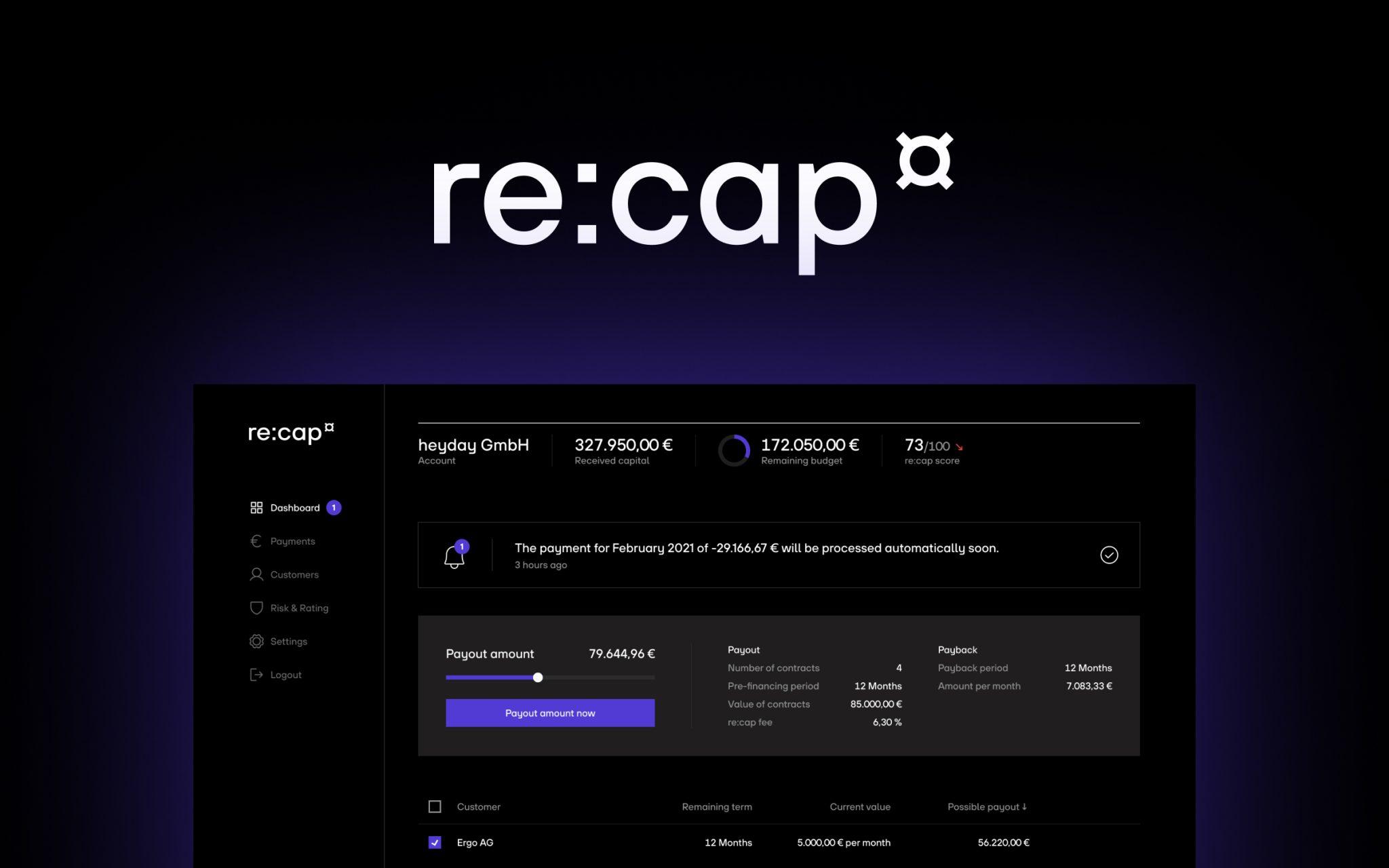

One to watch is Germany's re:cap, founded by fintech veterans Paul Becker and Jonas Tebbe, who previously founded LIQID — the fast-growing "wealth tech."

re:cap has today announced its $1.5m pre-seed round from the likes of Entree Capital. The round reportedly (soft)closed in just three days; an unusual feat for such an early round, hinting that investor appetite for this new space is sky-high.

"It was quite a spicy fundraise," Becker tells Sifted in an interview, calling Pipe a "role model."

re:cap, which has not yet launched, will initially only target German SaaS companies who have recurring revenue. However, Becker says the company, which will launch at the end of this year, has pan-European ambitions.

Other Europeans lining up to compete here are Bridg and Rail. Although still early-stage, they are both gearing up to take market share before Pipe expands into Europe.

So do the newcomers have what it takes? And is this the new hot trend to watch?

A new asset class

At their core, Pipe and its peers offer a savvy alternative to both traditional debt and venture funding.

Essentially, companies sell 'future revenue' as an asset to institutional financiers who buy that 'risk' and provide the forward capital at competitive prices. It's not technically debt — think of it more like a consultant getting their pay before they complete the job rather than after.

Fintechs like Pipe do the risk analysis and act as the middle man by offering a marketplace. Crucially, they are not the lender themselves, like Uncapped and Wayflyer, and focus on subscriptions as a guaranteed 'returnable.'

"I see us as a trading platform for a new asset class: basically, recurring revenue... That's why we're being pegged as the 'Nasdaq for revenue'," Pipe's cofounder Harry Hurst tells Sifted.

"Companies can trade revenue for upfront capital, trading with institutional investors [like Morgan Stanley]... We're giving companies access to capital markets. That's what sets us apart from other parts of alt-finance," he says.

To manage risk, the number of subscriptions that can be 'advanced' are capped (to allow for churn) and it's also limited to 12-month flows.

The gap in the market

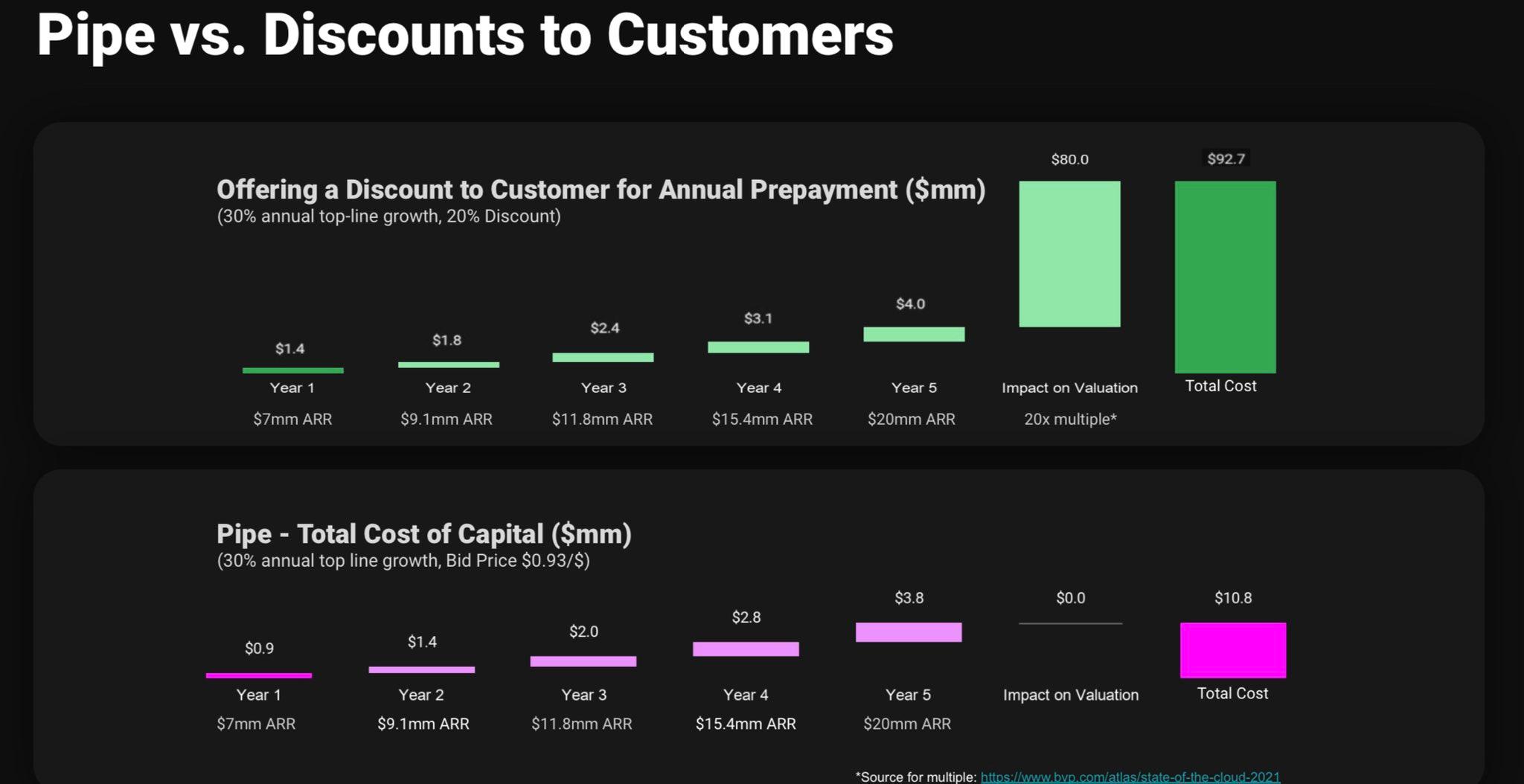

Currently, the main alternative for companies needing cash is to offer heavy discounts — sometimes up to 40% — on annual subscriptions, to incentivise consumers to cough up in bulk rather than by month.

"That is just inefficient," Becker from re:cap says.

Instead, re:cap offer companies a fee of between 5-15% to secure their subscription revenue upfront. It's more cash upfront (up to €2m), and at a smaller discount.

"When you scale, you need cash. The B2B financing space is not where it could be...but the technical infrastructure [now] allows for better financing solutions," Becker explains.

There's clearly demand — Pipe already counts 4k clients, from online pharmacies to food box services.

Unsurprisingly then, investors have been tripping over themselves to get in on his recent raise.

The irony, though, is that Pipe is pitching itself against VCs. Part of Pipe's ambition is to prevent founders from unnecessarily diluting themselves with venture money.

"Pipe is not an absolute alternative [to VC]...but we certainly displace the need for part of that," Hurst tells Sifted.

Becker from re:cap agrees: "We are another option [to VCs]... Maybe now you can raise $4m from VCs rather than $5m," he suggests, explaining that expenses like marketing should come from revenue not venture funds.

A pipe dream?

Given Pipe's success, it's unsurprising that investors are hunting for their own local moonshot that can rival the $2bn US fintech on home turf.

But there's a word of caution.

Tom Lambert from LocalGlobe says that investors need to be wary of saturation in Europe, having come across several Pipe lookalikes already.

"Entrepreneurs in Europe have woken up to the opportunity, having seen Pipe's early traction, and strong product market fit," he tells Sifted.

"But the question is — how are they going to differentiate? They're all competing for the same high growth startups, CAC [customer acquisition cost] is going to spiral. It's just a race to the bottom unless they can build in data insights."

European startups will also have to watch out for Pipe and its $150m war chest on home ground.

Hurst, a Londoner by birth and an avid tweeter, said a UK expansion was "in the works", although he declined to comment on timeline. "It's definitely a global opportunity," he added.

He has also come out fighting on Twitter on the subject of Pipe lookalikes.

For now, Europe is an open canvas. Becker even says he wants to "see Pipe come to Europe... There is room for several."

But it won't be long before this space becomes a land grab. It'll be the Europeans — fighting on home turf — against the US frontrunner.

A (nerdy) note

FYI, we did think about whether the 'revenue marketplace' model could be compared to supply chain financing, which has been tarnished by the collapse of Greensill.

There are parallels. In the 'revenue marketplace', companies seek money from customers that is not guaranteed but is near-certain. In supply chain finance, suppliers seek money they are owed by their clients, and is again near-certain (it's invoiced).

But Becker says there are two big differences.

First, in the re:cap model, suppliers' customers don't even know the marketplace exists. In addition, the marketplaces only service suppliers in the subscription economy, rather than logistics firms with ad-hoc invoices. The practicality of it is therefore fundamentally different.

In addition, as a marketplace, it doesn't provide capital off its own balance sheet — meaning they are not exposed to any risk directly.