The UK's top three digital banking apps have all now released their financial results for 2019.

By most accounts, it was a surly reality check for the sector, which has attracted millions of consumer users but seem to be struggling to control costs. Digital banks also still seem to be grappling with how to seriously monetise current accounts — often dubbed the "low hanging fruit" of banking — and it remains to be seen whether their business models can confidently ride out the coronavirus.

Still, beyond these shared trends, it's worth comparing how the three fintechs — Monzo, Revolut and Starling — performed in relation to one another.

Sifted also asked analysts and venture capitalists to share their top takeaways from the annual results.

The breakdown

Each of the fintech's annual results can be read in isolation at their corresponding websites or, in Revolut's case, on Companies House.

It's worth bearing in mind that each company follows slightly different reporting practices, and that these results are over 6 months old for the most part.

Revolut is also a slightly older company than the rest, launching in July 2015 in the UK, followed by Monzo in early 2016 and finally Starling in mid-2017.

Still, for ease, we have aggregated the core areas from each set of results below.

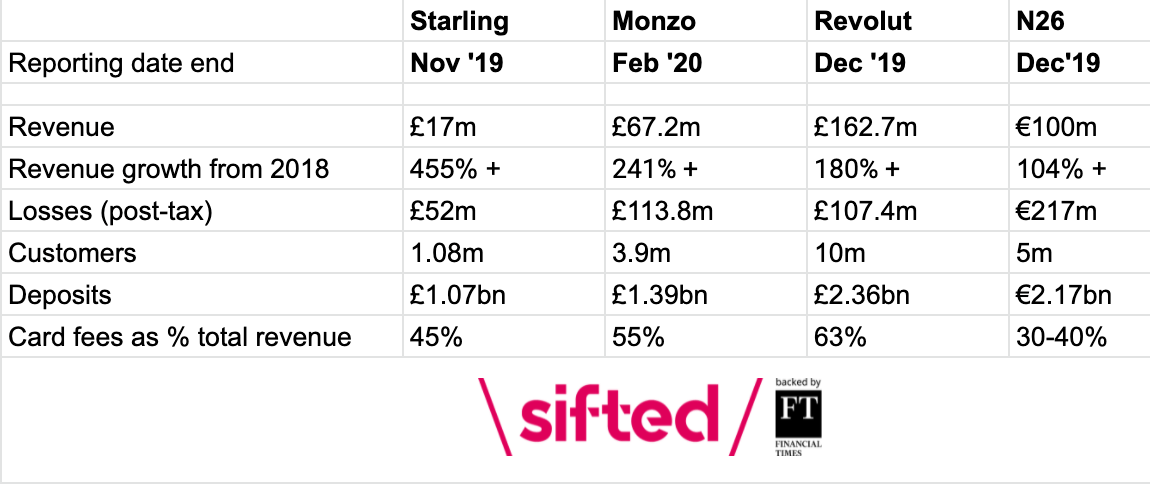

Starling has the most diversified revenue stream

Card transaction fees (known as interchange) still made up an important part of all three business models last year.

As noted above, 63% of Revolut's revenues came from interchange while 55% of Monzo's did.

But last year, Starling was the only one to have less than half (45%) of its revenues come from interchange, showing reduced dependence on a piecemeal income source that is ultimately pegged to how much people spend.

Instead, it also collected fees from its 80,000 business accounts, as well as having a handful of banking as a service (BaaS) customers, and from interest fees from lending and holding balances at the central bank.

Lourens Ruigrok, an investor at Finch Capital, praised Starling for having the most "sustainable" and least "fragile" revenue-model of the three fintechs. He also noted it was "more core to their customers."

However, Starling's marketplace model seems to have had disappointing results, bringing in just £72,000 in commission from connecting users to third party apps.

Revolut earns the most revenue per customer

By dividing revenue by the average number of customers in the year, you can get a rough estimate for how much each user generated in 2019.

In this area, Revolut led the pack, making £24 per customer per annum. It was followed by Starling with £21 and Monzo with £20.

This is partly because Revolut has the most customers, meaning it benefits from economies of scale, and also because it is most active in non-European markets where interchange fees are higher.

Fintech analyst Lex Sokolin says Revolut's revenues put it confidently in the lead. Speaking on the Rebank podcast, he said: "£160m in revenue... that number feels quite large and it does feel to some extent like a victory of building a large scalable business."

He added: "There is definitely a big performance difference that we're seeing between Monzo and Revolut, with Revolut pulling away quite significantly, £100m in revenue difference on the same burn number. And I think that's going to be tough for Monzo."

Revolut's ability to pull in paid users via its subscription service also shows that its users see value in them.

Sokolin also referenced Revolut's strength in pushing out new products quickly. He also estimates that Revolut squeezed out $5m–$10m in profit from their crypto-trading.

One investor, who questioned Revolut's valuation earlier this year, also said they were more bullish on the company after comparing its latest figures to that of its peers.

Still, to clarify, all three fintechs' revenues were burdened by losses involved in running and growing the businesses.

Moreover, in Revolut's case, the direct cost of running each account is still larger than the revenue each customer generates — meaning it still has a negative gross margin. That could force it to think about scaling back existing growth projects.

Meanwhile, Monzo has now lost one of its key revenue sources, after regulators stepped in to stop them charging a steep 50p daily fee for unplanned overdrafts.

Monzo is seeing improved cost-efficiency

One positive for Monzo is its revenues are rising faster than costs.

Monzo's revenue grew by 241% year-on-year, while its cost-base increased by only 159%. To put it another way, for every £1 spent in 2019, Monzo generated 37p; up from 28p in 2018.

Monzo's unit-economics has improved such that each account now generates £4 in profit a year on average, when accounting exclusively for client servicing costs (rather than total costs, which include everything from salaries to marketing). This is a vast improvement from the net loss per account of £15 they recorded in 2018.

In contrast, Revolut's cost-efficiency actually dropped. In 2018, it generated 64p per £1 spent, but in 2019 it dropped to 61p.

Starling holds the most deposits per customer

Collectively, the three challenger banks held £4.8bn in customer deposits at the last count.

That still makes them very small. By comparison, Virgin Money, one of the previous crop of “challenger” banks, has around £64bn in customer deposits; and Metro Bank has customer deposits of £14.5bn.

Still, one important point of comparison for Starling, Monzo and Revolut is how much money users deposit on average.

Starling leads here, pulling in £999 per user at the last count; largely due to its headstart in business banking, where deposits tend to be larger.

Monzo is now in second place, increasing its average user deposit rate to £357 from £142 in 2018.

Meanwhile, Revolut has dropped from having an average deposit of £252 per user in 2018, to £236.

Starling is growing fast

Starling is also technically acquiring customers the fastest in the UK, when adjusting for its later launch, as shown in the graph below. This reflects the fintechs' pace of growth in their home markets from their launch date.

Note, this does not illustrate the rate of active customers or the churn rate for each fintech; data which is difficult to access.

Nobody won on lending

Both Monzo and Starling began lending last year (Revolut is not a UK bank so cannot lend off its own balance sheet).

Yet Marc Rubinstein, a former hedge fund analyst calculated that "lending is hurting" the banks, with predicted losses outweighing the interest they earnt from loans last year.

For instance, Starling recorded £2.1m in interest income from customers but has £2.2m in provisions for bad loans.

As a result, Rubinstein concludes that Starling and Monzo would "have been better off not lending a penny" in 2019; particularly Monzo, who he shows below has a much riskier loan book than Starling.

Moreover, Finch's Lourens Ruigrok told Sifted that digital banks will now have to resist pressure to grow their loan books at all costs.

"Lending seems to be the most obvious opportunity to monetise but has its challenges. Strong knowledge of how to effectively lend money and run a healthy loan book are key and loan books don’t scale like VCs want them to."

Still, Starling says its lending book has already grown rapidly in the financial year of 2020, thanks to its role in deploying government-backed loans.

Note; the reports do not make clear how much the banks actually had in realised losses from loan defaults.

Worth their valuations?

Analyst Lex Sokolin argues none of the fintechs' unit economics are particularly compelling relative to their valuations.

"If you look at the unicorn valuations of these companies, they are pricing on a per user basis valuation somewhere like $1,000...in enterprise value per user. So you take the 5 billion [dollar valuation] divided by the number of customers," he noted, speaking on the Rebank podcast.

"The reality is all of these companies are making 20 to 30 bucks a year per customer. And so for me that's the core existential question; how do you go from 30 bucks a year per customer in revenue probably at a loss to 1,000 bucks per customer in enterprise value?"

He concluded:

"Are these banks at all or are they media companies with financial services monetisation?"

Unfortunately for Monzo, given its burn rate and the size of its recent fundraise, it will be the first to put this question to investors again.