Buy-now-pay-later (BNPL) platforms like Klarna have never been busier or more lucrative, with lockdown increasing shoppers' demand for credit.

And now there's a new player in the frame; Zilch, a London-based fintech backed by Gauss Ventures, promising a "responsible," handy alternative to BNPL.

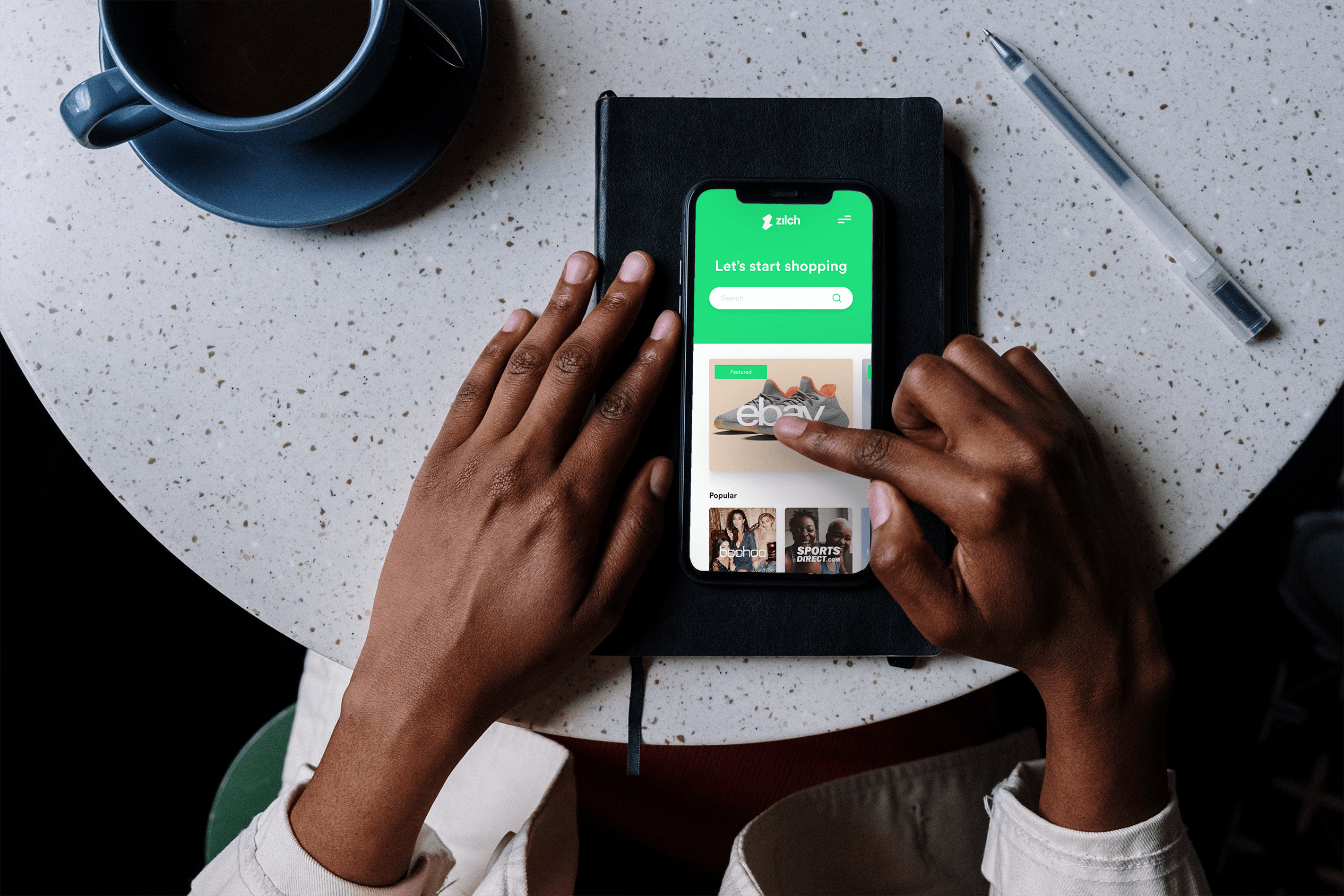

Zilch has launched what it dubs "an American Express for millennials and Gen Z", offering users a card with a personalised credit line which is then paid back in instalments.

The youth market has proven to be a hot new space for fintechs, with players like Revolut, Kard and Zelf all hungrily tapping into teenagers and the 18-24s.

If Zilch succeeds, it could eat into the profits of both BNPL providers and traditional credit cards. The fintech could also compete with another of Gauss' portfolio companies, Curve, which is set to launch its own credit line.

Zilch has seen good progress since going live in 2019, announcing Monday that it had won a rare consumer credit license from the UK regulator, the FCA.

The company, which has raised over $10m, says it is already growing at an average pace of 1,000 new UK sign-ups a day.

It's now looking to boost its numbers further via a mass "fin-influencer" campaign, following in the footsteps of digital finance apps Bo, Revolut, and infamously — Lanistar.

Shedding light on the marketing strategy, Zilch's chief executive Philip Belamant said:

"We'll only use Zilch ambassadors. Those who know and love products."

Customer-first

The idea behind Zilch is to be a seamless, interest-free lender.

CEO Belamant says that existing BNPL players like Klarna are cumbersome, disrupting the checkout process when credit is denied and only being available at set merchants.

"BNPL has been built for retailers, not the customer," Belamant told Sifted. "We wanted to give the same benefit to the customer, but make it customer first and retailer second... You don't have to worry about getting rejected at the very end now. And you can shop anywhere."

Having a single card also saves consumers from handling multiple BNPL providers, including Afterpay, Clearpay, and France's Alma.

"The market is fragmented. You're shopping on one site today, and another tomorrow...[BNPL players] don't talk to each other. So Zilch consolidates that onto 1 platform."

In many ways, this makes Zilch more like a standard credit card than a BNPL platform. But unlike credit cards, Zilch has no interest or late fees — or"15 pages of small print."

"It’s all the convenience of a credit card, and all the transparency of buy now pay later," explains Belamant.

Rather than charging consumers interest, Zilch instead makes money via interchange fees and from affiliate partnerships on its app (for instance, recommending products to shoppers on the Zilch platform). Using credit at any non-partner merchant also costs £2.

The card is currently only available online but is set to be for in-store soon.

Zilch's tagline is "Have what you want, when you want it" — is this not encouraging the same spendthriftiness as Klarna?

Responsible?

Zilch stresses it has customer wellness at its heart.

The company says the right "questions are being asked" of players like Klarna and how far they stretch consumers' borrowing capacity.

In response, Zilch says it's calculating credit lines not just based on loan riskiness, but also on users' affordability. That means calculating how much shoppers can really afford to spend, driven by open banking data (as well as credit bureaus).

Belamant says Zilch's ethics are also reinforced by its business model, which asks users to pay 25% per purchase upfront and doesn't rely on excessive spending.

“We’ve gone the other way round [to BNPL platformers]. Retailers bid against each other to get more or less exposure on the Zilch platform," rather than hunting to find the lowest transaction fee.

Nonetheless, given Zilch's tagline is "Have what you want, when you want it" — is this not encouraging the same spend thriftiness as Klarna?

"Well...we started with ‘responsibly have what you want, when you want’, but it didn’t sound as good," Belamant laughed.

Evidently, Zilch taps into consumers' desire to buy beyond their immediate means.

But what's positive, at least, is that Zilch will request access to users' financial data. This offers an extra layer of protection that most BNPL players omit, with 78% of Zilch customers agreeing to share their data.

Belamant also stresses that Zilch is the first BNPL product to win a license from the FCA. Most other BNPL players operate in a "regulatory void," he says, while Klarna is regulated in its native Sweden.

Zilch, which now has 33 staff based in London, is set to close a Series B to the tune of $50m next year.

Chief executive Belamant is a serial entrepreneur and mobile-payments expert, having founded a Top 40 Fintech company in South Africa.