Startups that land in VCs’ laps via so-called ‘warm introductions’ are 13 times more likely to be funded by them than startups which come to their attention via ‘cold’ pitch deck submissions, finds a report published this week by Diversity VC and the British Business Bank.

Check Warner, CEO of Diversity VC, a non-profit organisation promoting diversity in tech, says that the importance of introductions from contacts is “really damaging” for the diversity of the UK’s tech sector.

Not only does it reward those who are already tapped into networks, but startups with all-female founding teams reap less benefits from these warm introductions than all-male female founding teams.

“Founders without links to a VC are at a significant disadvantage,” says Warner. “It means that the VC industry is restricting the flow of new ideas to only those that are already in their networks. Not only are female founders missing out, but so are investors.”

While the tech sector is growing five times faster than the rest of the economy, it’s not addressing its often-highlighted diversity problem at such speed: rather, the pace of change is achingly slow. Female founders are under-funded and underrepresented, and have been for the past 10 years.

For every £1 of venture capital investment in the UK less than 1p goes to all-female founder teams, 10p goes to mixed-gender founder teams, and 89p goes to all-male founder teams.

Warner thinks VCs need to open up to address the issue. “There needs to be more opportunities for diverse founders to meet investors, such as a weekly 'office hours' meeting sessions. Firms also need to take seriously introductions that come in ‘cold’, from outside their networks.”

It would also help, she thinks, if VCs were themselves a more diverse bunch. “87% of the decision makers in UK VC firms are male, so warm introductions are, by definition, more likely to be made to male partners, who may find it easier to connect with businesses founded by people like them (otherwise known as affinity bias). Following the initial introduction, the chances of affinity bias increases as the company progresses through each decision-stage.

“It is clear that the venture capital sector will access a better and wider range of opportunities if their own teams become diverse, especially at senior levels.

“Finally, investors need to get better at being specific about what they are looking for, so founders know exactly what will appeal to them without needing an initial introduction or meeting. This will make 'cold' approaches far more appealing for everyone involved.”

Here are the five charts my colleague Max Traeger found the most interesting:

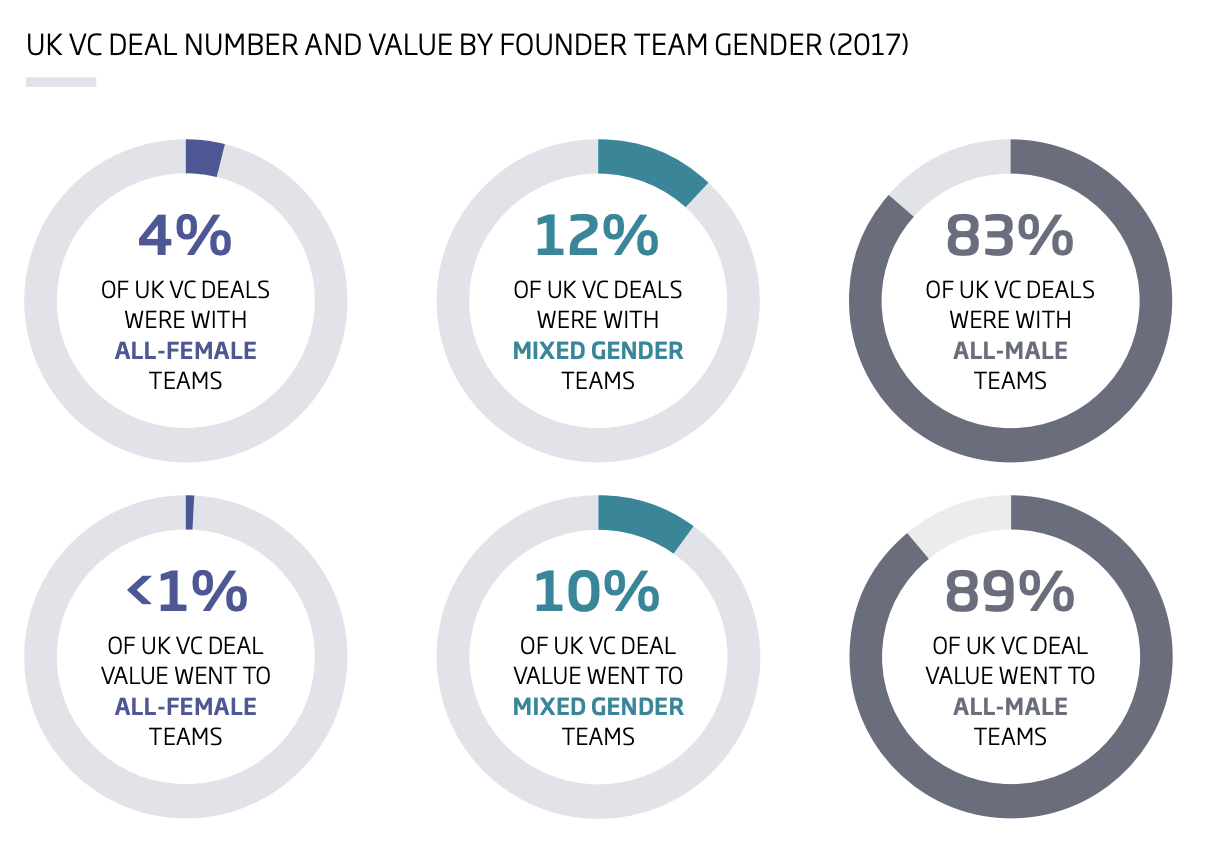

1) The vast majority of VC deals go to companies with no women on their team

All-female teams took home just 4% of the total UK VC deals in 2017, less than 1% by value.

Mixed gender teams did slightly better – gaining 12% of deals, or 10% by value. Collectively, around 17% of all UK VC deals in 2017 – just 11% by value – went to companies with at least one female founder.

These numbers are similar to findings in the US, where 17% of all deals went to firms with at least one female founder in 2016 and 4% of all deals (2% by value) went to all-female teams in 2017.

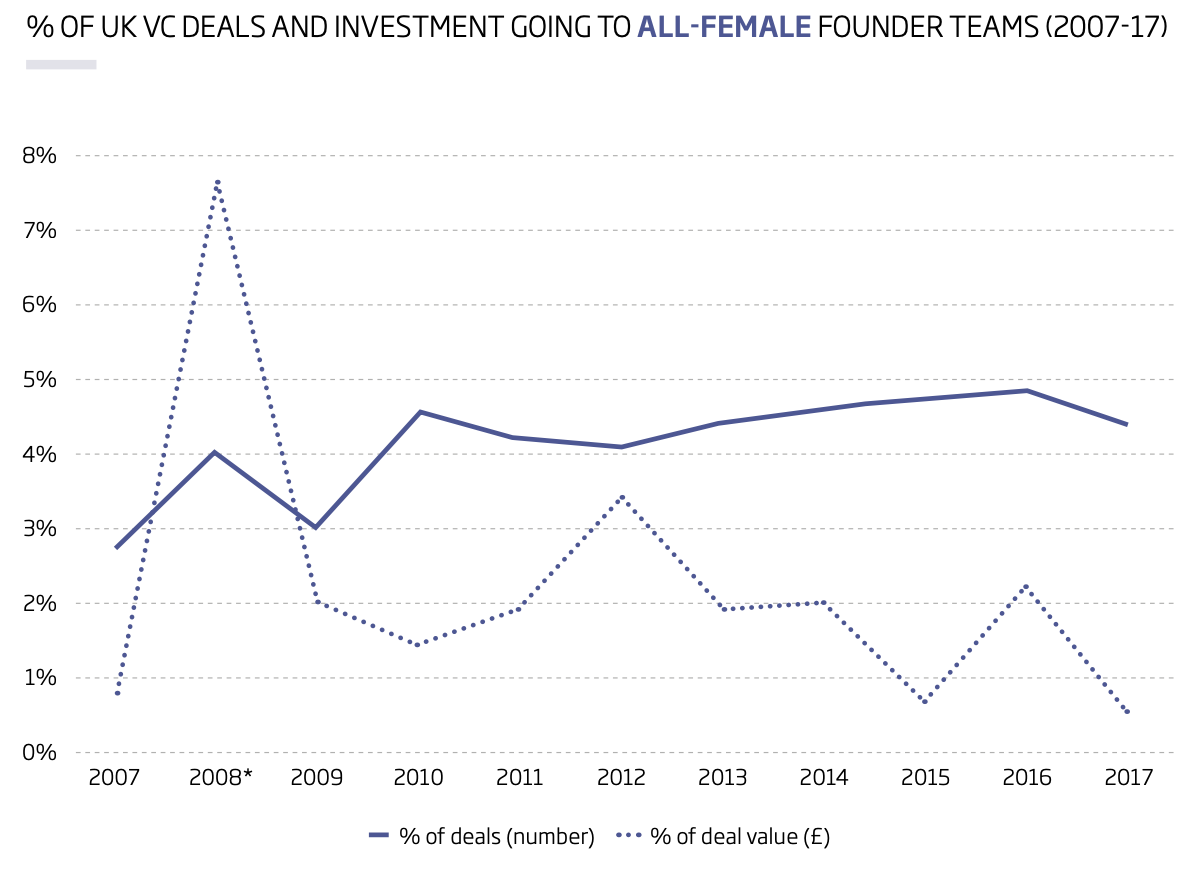

2) The percentage of deals for all-female founding teams is (slowly) increasing

It is true that the bare-bones numbers of VC deals in the UK for all-female teams have grown from 7 deals in 2007 to 39 in 2017.

But, as a percentage of the total deals, improvement is pretty sluggish. This pattern rings true for investment value where, despite investment into all-female teams increasing from £5m in 2007 to £32m in 2017, there has been a decline as a proportion of overall investment.

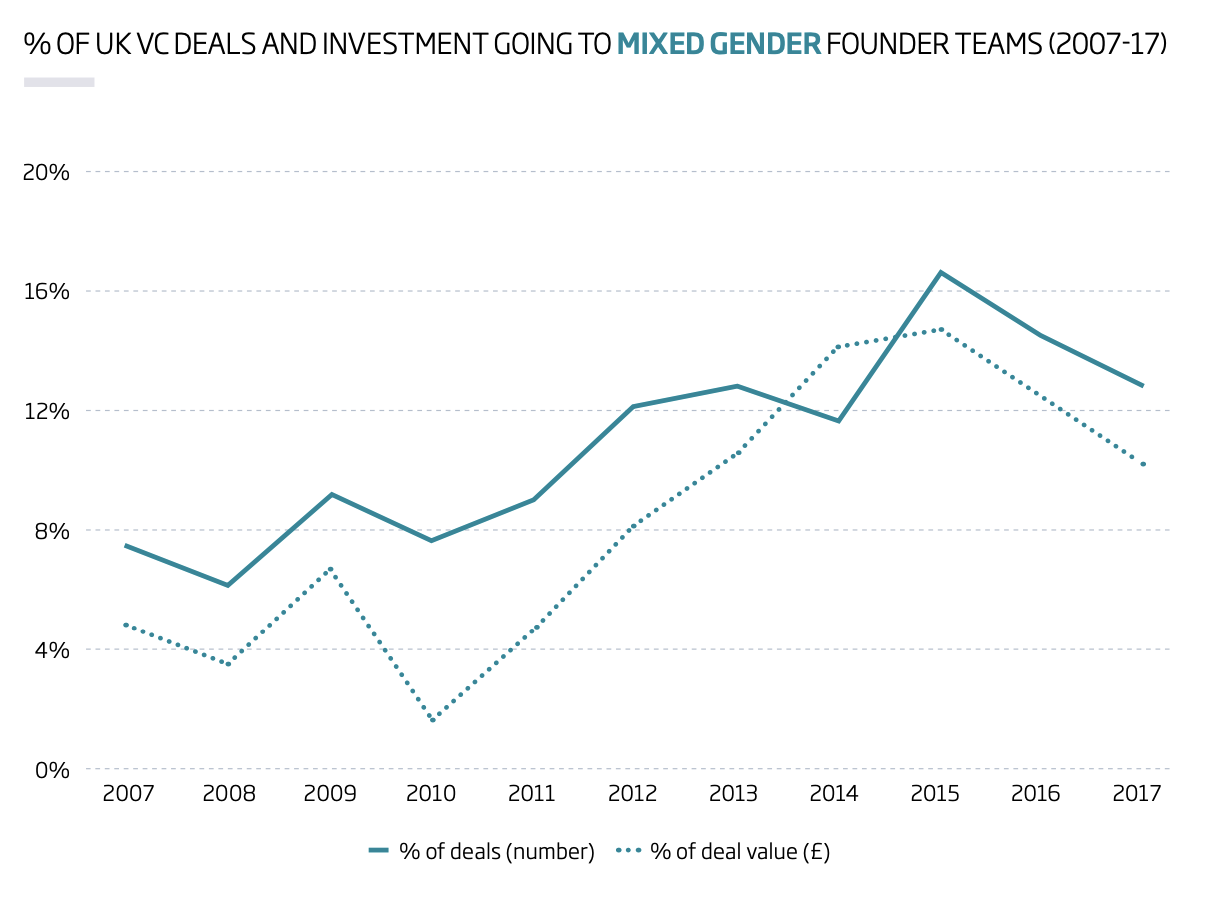

3) With mixed gender founding teams, the proportions are better, but still weak

For mixed gender founding teams, the proportion of UK VC deals they win has risen from 7% to 13% in the past decade.

For investment value, the percentage is growing roughly in line with the number of deals, reaching 10% in 2017. This is still unacceptably low. For comparison, 49% of all SME employers have a mixed gender leadership team, and 19% have a female majority.

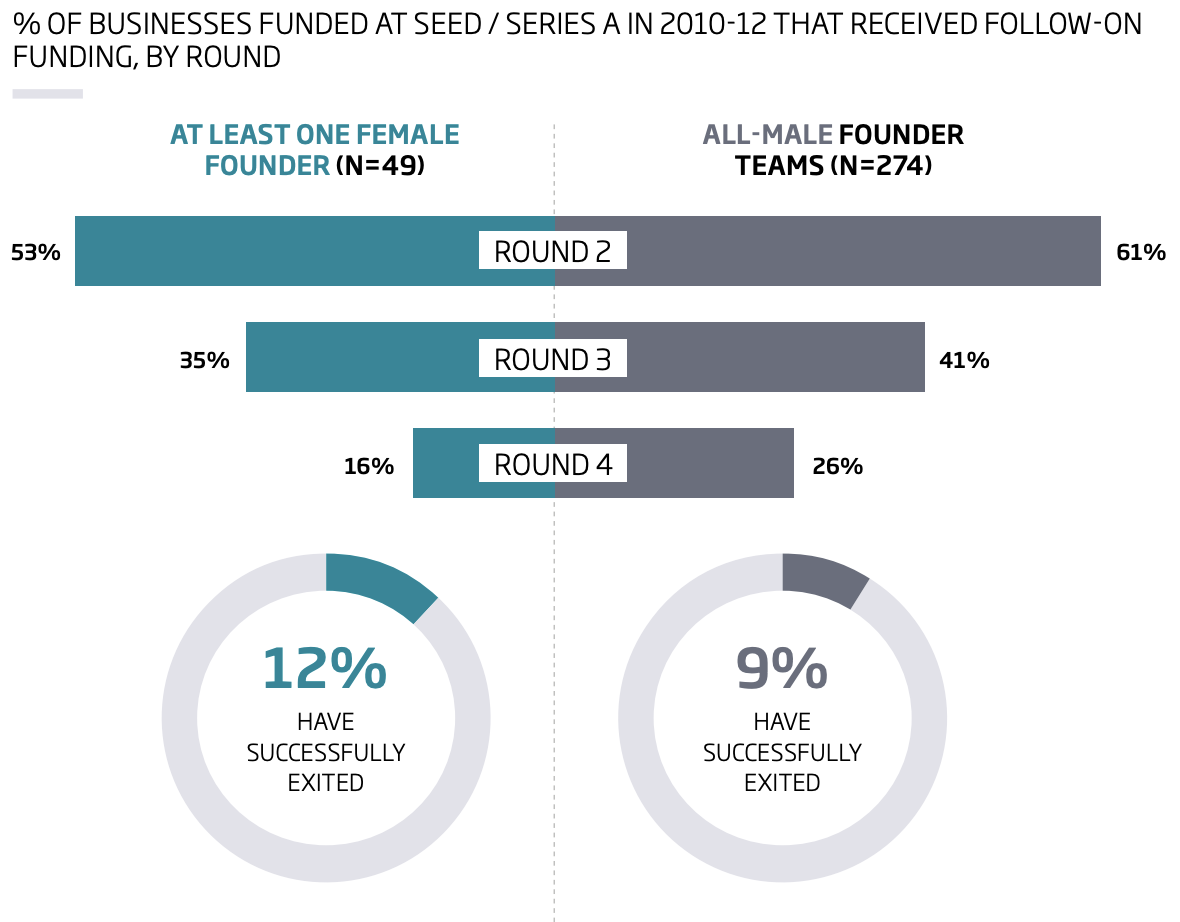

4) Companies with at least one female founder are less likely to receive follow on funding but more likely to have exited

Looking at this chart it is clear that of the companies winning seed/series A funding in 2010-12:

- 53% of companies with at least one female founder won a second funding round;

- 61% of companies with all-male founders won a second funding round.

This effect has persisted in subsequent funding rounds.

For the same cohort of companies:

- 12% of the companies with at least one female founder have successfully exited (as of April 2018)

- This compared to 9% of all-male founded businesses.

Industry differences could explain the variation in follow-on funding and exit rates (e.g. businesses with female founders may be more likely to be in industries which require fewer funding rounds or exit earlier).

5) The pace of change is slow, very slow

The most sobering finding in this report for all those in the industry working so hard to improve gender representation is that the rate of improvement is desperately slow.

In the decade between 2007 and 2017, the rise from 2.7% to 4.4% adds up to only 0.2 percentage points per year. At this embarrassing rate, it will take until 2045 for even 10% of UK VC deals to be in female teams.

As more and more reports come out, it has become undeniable that the startup and VC sector is extremely homogeneous. In Europe in 2018, 93% of founding teams which raised money had all-male founding teams. Only 6% of CEOs in Europe are female, and 1% of CTOs.

This report has indicated how much further the VC industry has to go in promoting and supporting female entrepreneurs to win funding.

Lack of diversity is not only a social imperative, but it is also holding the industry back from performing as well as it can. It is clear radical change is required.