The good news: Europe’s tech sector is coming back to life. The bad news: it’s doing so kind of slowly.

“We’re seeing a gradual recovery; it’s no hockey stick,” says Sonya Iovieno, head of venture and growth at HSBC Innovation Banking. “Investors are opening up their wallets more than last year — but there has been a flight to quality, so at Series B and beyond, companies have to be the ones outperforming their class and peers [in order to raise from new investors].”

But one area where things are really picking up across the board? Venture debt funding.

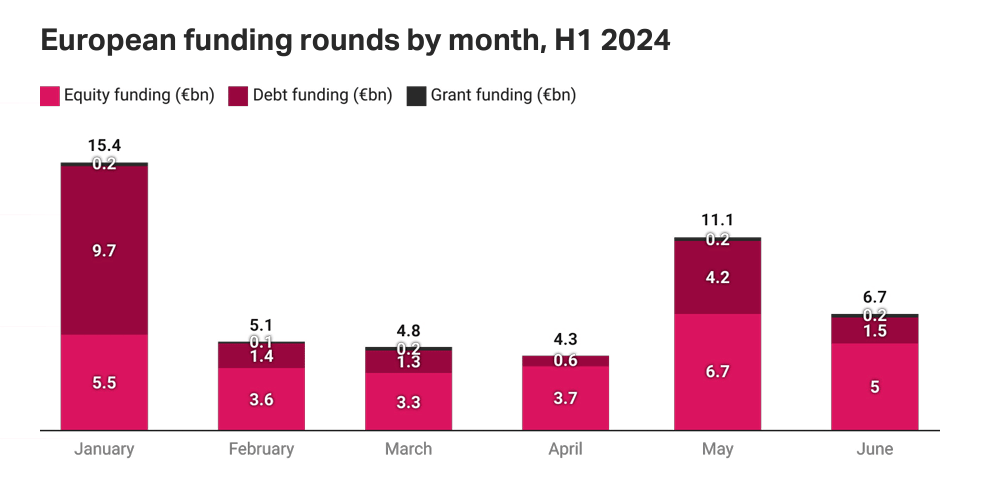

In the first half of 2024, European startups raised €18.7bn in debt funding, according to Sifted data. If things continue at the same pace for the rest of the year, it will set a new record.

That, in turn, is a sign that M&A activity should pick up over the rest of the year — and definitely in 2025. “It’s early days for M&A — we haven’t seen as much activity as we would have expected — but, given the types of debt rounds we’re currently writing, I expect we’ll see a pick up.”

What’s driving debt deals?

“Companies are being cautious in the current economic climate,” says Iovieno; many are raising debt to “bolster the balance sheet and add an additional runway buffer”.

Others are being opportunistic. At Series C and above, many companies have an M&A strategy in play, she adds — and are setting up “hunting lines” for potential future acquisitions, or raising debt to make a specific acquisition. “They’re getting the prices they need [now] in order to engage in M&A activity,” she adds.

There are bids already underway in the enterprise software sector; large corporates are looking to buy startups — so too are PE firms, says Iovieno.

“We’ve also seen quite a bit of M&A in AI, although it’s still quite early,” she says. “For the most part it’s something about the tech stack or model that makes it worthwhile to make the acquisition, as a small bolt on for a Series B or beyond company.”

Elsewhere, startups are “running out of runway” and becoming easy targets. “There are some good deals to be had on the consumer side,” says Iovieno. “A few of them are running out of capital and haven’t reached profitability.”

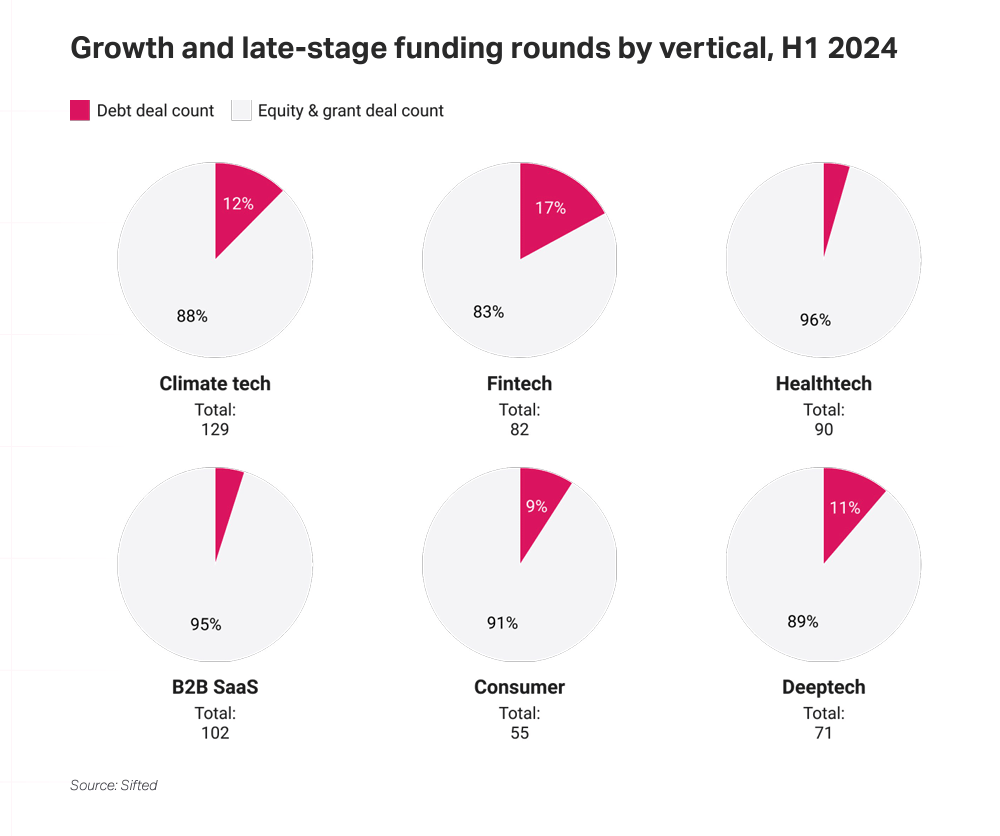

Climate tech is where it’s at

Venture debt is flowing towards the climate tech sector in particular.

“The last two years there’s been a lot of excitement around climate, but people were not quite sure where the growth drivers were going to be, or what the commercial model would be. A lot of those questions have been answered as companies got commercial contracts, and that helped normalise the metrics investors are looking for, which helped them attract equity,” says Iovieno. “It’s a real growth area.”

Fintech has also “come back strongly”, she adds — both debt and equity.

Debt not such a dirty word

It’s becoming more common for European companies to raise debt, says Iovieno — but it’s still not routine.

“In the US there’s almost an expectation to put debt in place as soon as you raise equity. We’re starting to see that behaviour in the UK and Europe, but it’s still a developing class here.”

It’s also becoming more common for startups to announce debt funding, adds Mat Gazeley, HSBC Innovation Banking’s public relations lead. “In the last two-to-three years, we’ve seen much more willingness and openness to talk about it.”

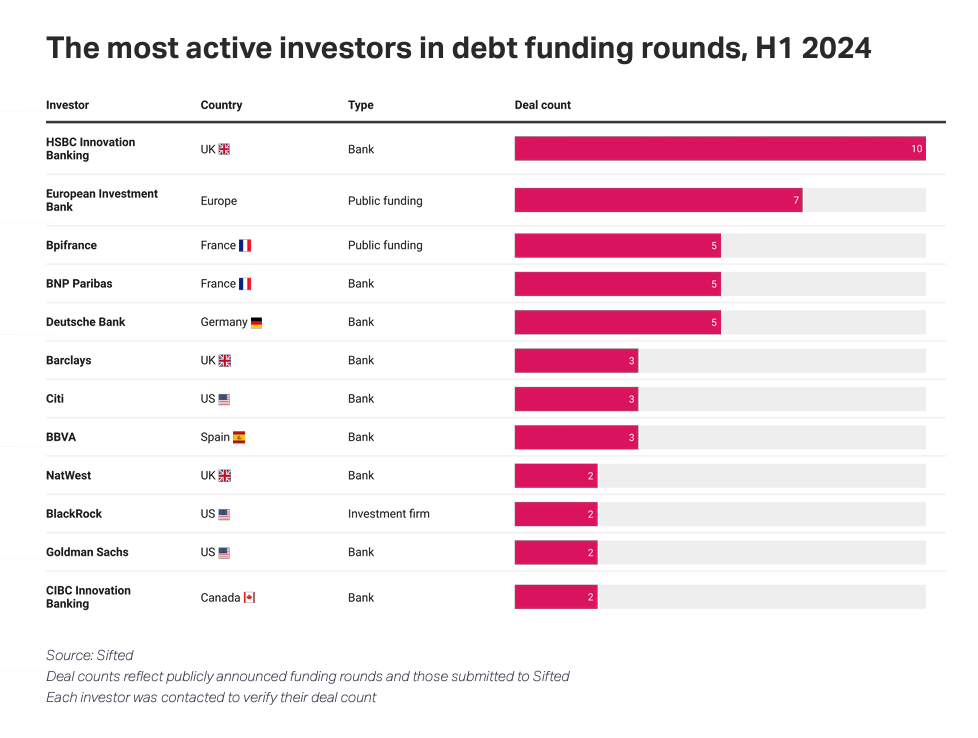

So far this year, HSBC Innovation Banking has publicly announced 12 debt facilities, totalling around $883m — and done several more undisclosed deals. That makes it Europe’s most active venture debt provider of the year so far, per Sifted data.

European VCs are also eyeing up debt funding — but few have taken the plunge so far. “We know VCs in Europe have looked at it, and so far haven’t really leant in — it’s a very different class,” says Iovieno. “We’ve seen a few North American banks dip in and out [of Europe’s debt landscape] and some UK banks coming in… but they’re less comfortable with the Series A or B stage.”

What’s next?

“Interest rates are still holding back valuations. [When they shift] that will be the next moment when you see an unlocking of the markets again — across M&A, equity and debt deals.”