General purpose artificial intelligence is increasingly becoming a game for Big Tech and Big Government in the US and China, leaving Europe trailing in the dust. But AI is also a game for nimble startups that can creatively apply the technology to particular business niches, giving Europe a chance to flourish.

Those are two of the main takeaways from the third annual 176-slide State of AI report, written by Nathan Benaich and Ian Hogarth, two of the most active angel investors in the UK in AI startups. They also highlight the investment momentum that is building behind European AI startups in the life sciences and military fields, in particular.

One of the most striking features of AI research, as shown in the report, is how it is being driven by huge amounts of capital, data and computing power, meaning that only the biggest players can lead in many fields.

The biggest companies also have the ability to hire many of the smartest research brains. Google, Amazon and Microsoft have hired 52 senior AI researchers from US universities between 2004 and 2018.

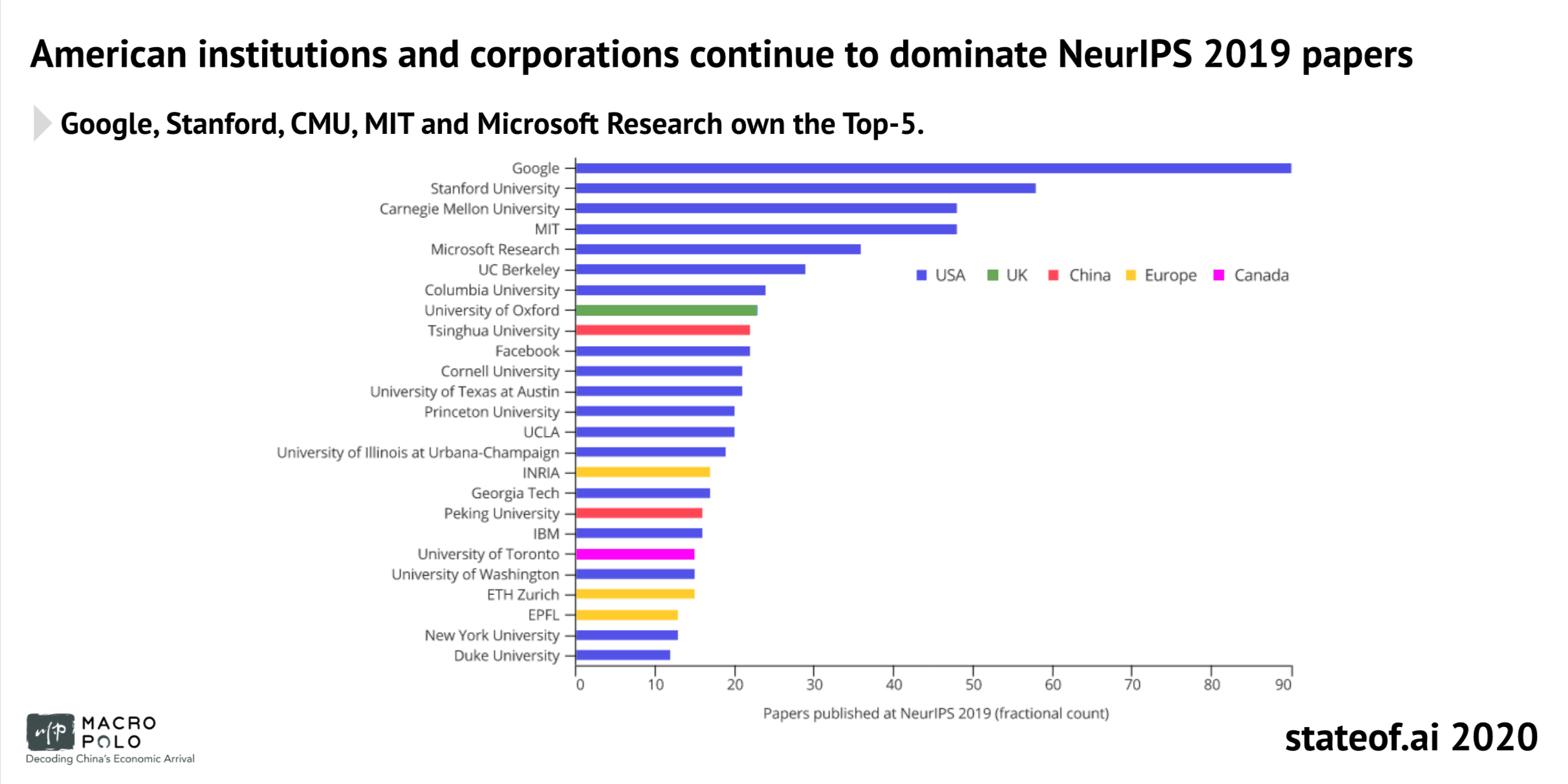

Unsurprisingly, US institutions and corporations present the most papers at the prestigious NeurIPS conference each year. The top five are Google, Stanford, Carnegie Mellon, MIT and Microsoft Research. Only two European institutions (Oxford University and INRIA) make it into the top 20.

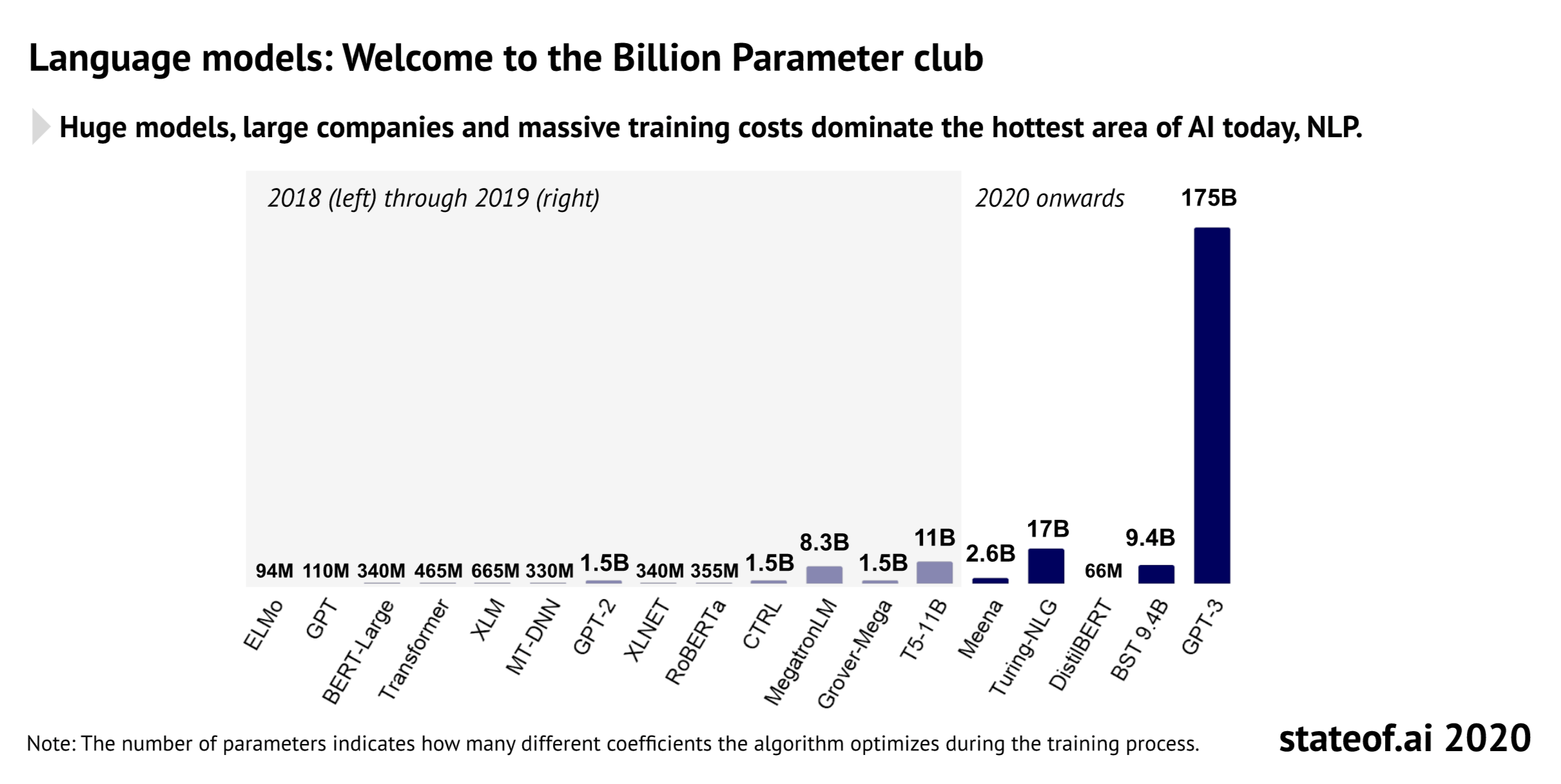

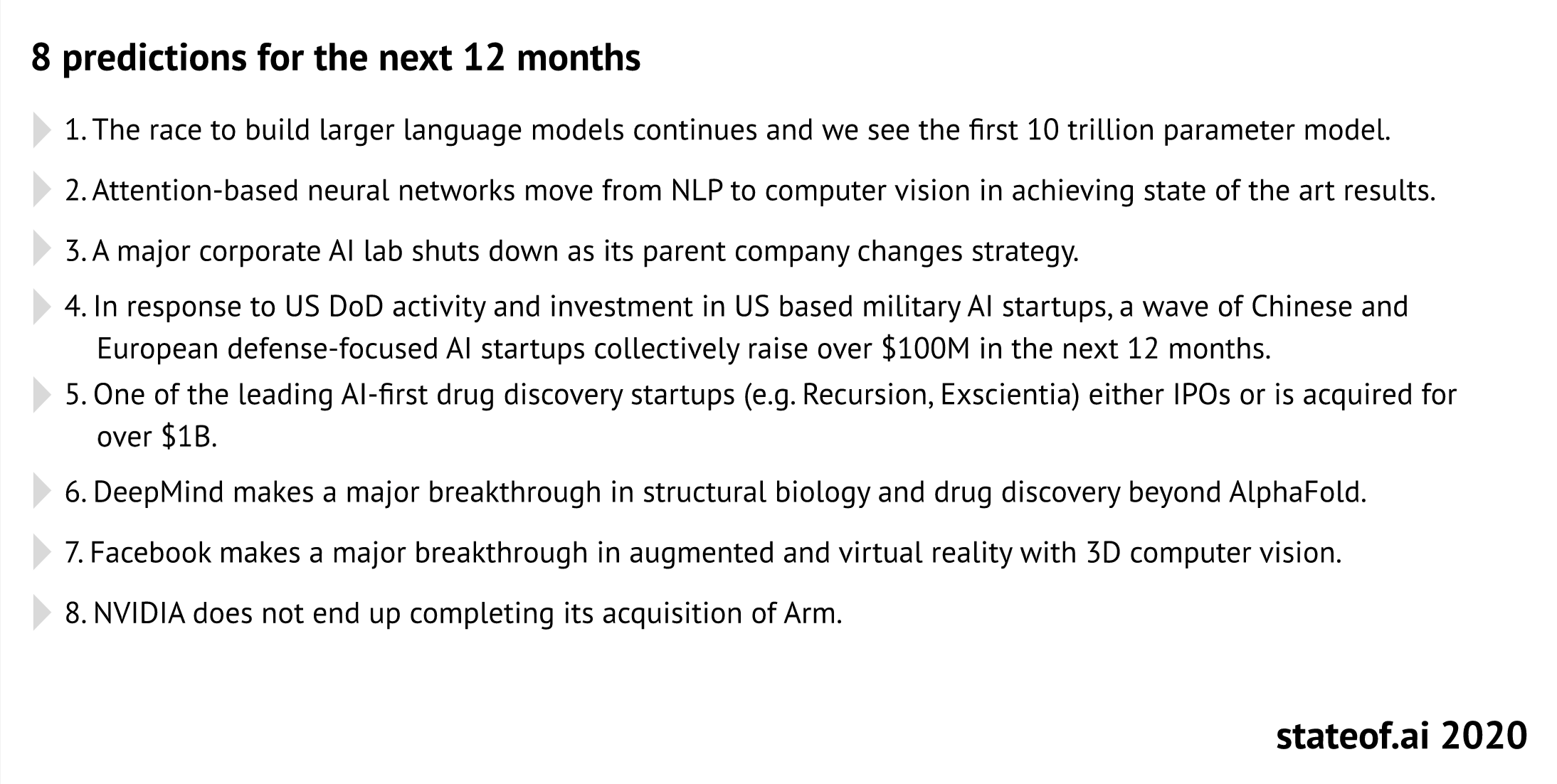

The report suggests it probably costs OpenAI about $10m to produce GPT-3, the deep learning language prediction model that can produce startlingly good text and has been the talk of the AI world this summer.

However, some AI researchers argue that progress in mature areas of machine learning is stagnating because of the massive inputs required.

“We are rapidly approaching outrageous computational, economic and environmental costs to gain incrementally smaller improvements in model performance,” the report says.

In spite of the dominance of the US and Chinese tech giants, the authors see plenty of opportunities for startups to apply AI, often using open source machine learning libraries, such as Facebook’s PyTorch and Google’s TensorFlow.

“The big companies are focused on general purpose models. But startups are focusing more on the engineering and building models that deliver customer value. We are looking to invest in niches that can become the next dominant paradigm,” says Benaich, who is a general partner of the VC fund Air Street Capital.

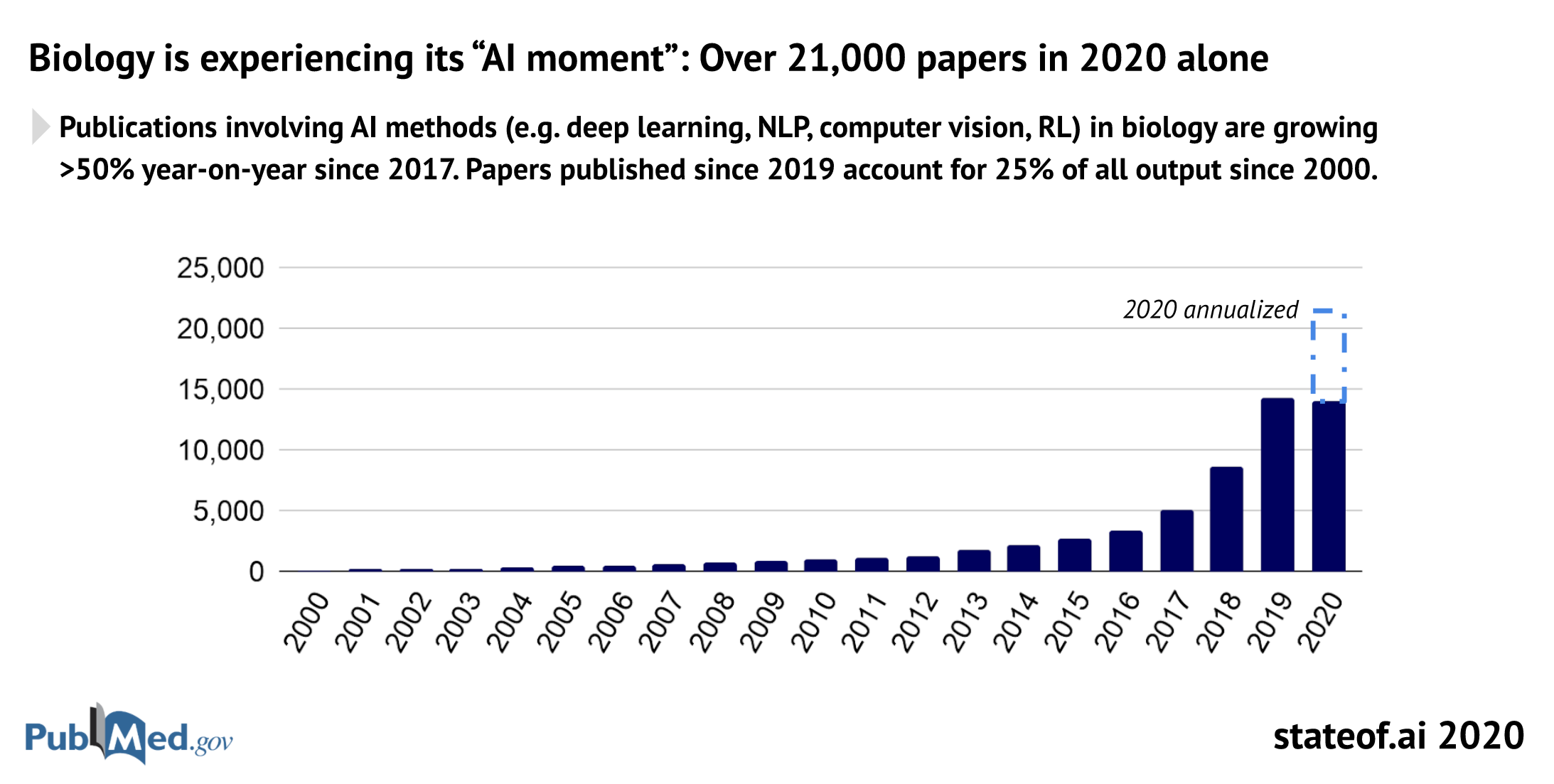

He suggests that there are rich opportunities in the life sciences area as “biology is experiencing its AI moment.” He points to the example of Exscientia, the Oxford-based pharmatech company that is using AI to accelerate drug development.

One of the other hot areas for investment identified by the report is military AI. Somewhat unnervingly, the US is making big efforts to apply the latest AI techniques to military ends. Last month, an AI “pilot” consistently beat one of the US Air Force’s best F-16 top guns in a simulated aerial dogfight.

The report predicts that Chinese and European AI-focused defence startups will collectively raise $100m in funding over the next year.

It also predicts that we will see even bigger language models emerging over the coming year (10tn parameters compared with GPT-3’s 175bn) and that there will also be significant improvements in computer vision. Interestingly, the authors suggest that for political reasons Nvidia will not complete its acquisition of Arm, the Cambridge-based chip designer.

Hogarth, the co-founder of Songkick who has now invested in more than 60 startups, rejects the argument that Europe is “losing” the AI race, made by the Chinese tech entrepreneur and author Kai-Fu Lee in an interview with Sifted.

But he suggests that Europe does have to give its emerging AI startups more firepower to compete globally. “I strongly and respectfully disagree with Kai-Fu Lee that Europe is out of the game. But we still lack the confidence and conviction to back our champions,” he says.