Swedish state-owned pension funds are putting aside billions to invest in the growing startup sector through VC funds. According to the recent State of European Tech report by London-based VC firm Atomico, Nordic pension funds account for 16% of total VC funds raised in the region since 2013; in Sweden, the share is even higher.

Investments from pension funds have helped Swedish VC companies raise larger funds than otherwise possible. Back in 2016 Northzone, an early investor in Spotify, was able to raise its biggest fund so far of €350m, thanks to investment from state-owned pension funds AP3 and AP6.

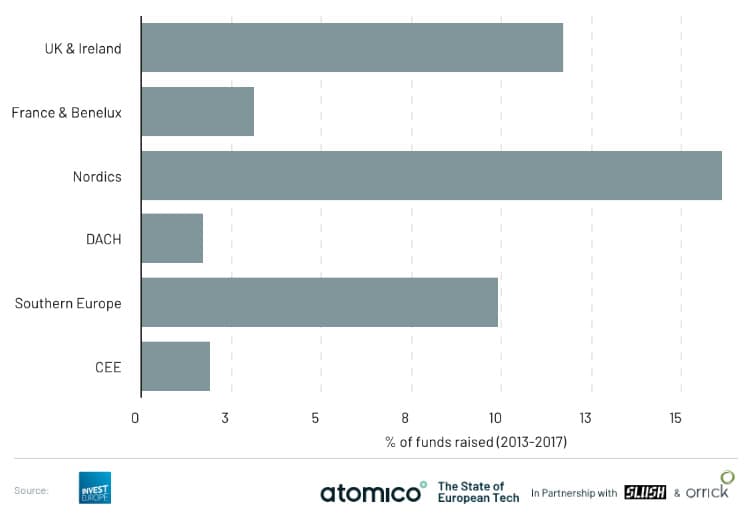

Nordic pension funds account for 16% of total VC funds raised in the region since 2013

”For the last six or seven years, we have seen a big shift in how the Swedish pension funds invest in VC. Since the early 1990s investments in private equity, or alternative investments as they are called, have increased; as PE has grown and become more fragmented, investments in VC have gradually grown,” Pär-Jörgen Pärson, partner at Northzone, explains.

German pension funds steer clear of VC

In Germany, where five of Europe's top 10 corporate investors can be found, it’s a different story; pension funds’ investments in VC only account for a small percentage of VC funds raised. In Germany, Switzerland and Austria pension funds only account for 2% of the total VC funds raised since 2013.

This is due to a number of factors, according to the long-term investment advisor and managing partner at Adina Capital in Hamburg, Holger Seidel.

”It has partly to do with the transaction costs. On the one hand, it takes a lot of effort, time and knowledge of the ecosystem to do this kind of investment. On the other hand, the capital that can and should be invested in VC funds are not huge amounts, which means that a lot of resource is required to deploy a small amount of money,” he says.

For the Swedish pension fund AP6, which is solely focused on investments in unlisted companies, 16% of its overall fund was allocated to venture capital in 2017, which adds up to €345m.

”We have invested in VC for quite some time; when for example [Swedish investor] Creandum raised its first VC fund 15 years ago we were there,” says Karl Falk, Head of Fund Investments at AP6. ”Since then we have invested in a number of VC funds, including those of Atomico and Northzone.”

It takes a lot of effort, time and knowledge of the ecosystem to do this kind of investment

Because of the strict Swedish law that the state-owned pension funds are governed by, AP6 is the only one that is allowed by law to invest directly into non-listed companies, and can therefore circumvent the VC funds; for 2017 these direct investments equaled more than one-third of AP6’s overall investment in VC.

”Sometimes a VC firm is looking for a partner that is able to not only invest in its fund but also co-invest in one or more of their companies. And with these direct investments we can reduce the management fees that we would otherwise incur,” Falk says.

Impatient investors

In Germany, where the pension funds are privately owned, the question of annual returns is important, according to Seidel.

”For the chief investment officer, it is often a lose-lose situation to invest in VC funds. Whilst other types of assets can quickly show positive results, this kind of investment can take several years before that happens and as a CIO you will constantly have to describe the J-shaped growth curve for the board and why it is a good investment,” he says.

”It can also hit individual CIOs hard when it comes to annual performance. Sure, they may get the returns five to 10 years from now but who is to say that they will stay in the same position for that long?”

That alone cannot explain why the difference between the two regions is so great. According to Seidel, it also have to do with differences in how to look at previous performance. One reason why the German pension funds are more apprehensive when it comes to VC investment is due to the need for previous track records. Since VC have not been that common previously, the earlier performance of VC can be difficult to draw conclusions from.

For the chief investment officer, it is often a lose-lose situation to invest in VC funds

Falk points to the small markets in the Nordics and how both companies and funds have had to look globally from day one to be able to grow and to get good returns. In comparison to Sweden, Germany and France have already huge home markets, which in turn has led to better international know-how among Swedish pension funds.

”Over time we have broadened our geographical focus to include Europe and the US. We have a proactive approach to mapping VCs in these markets and each investment is preceded by a very careful due diligence process based on our own evaluation methodology. We have had good returns the last few years but we have to see these as long-term investments,” Falk says.

Risky business

The risk of investing in startups is greater than other types of asset classes; however according to Swedish pension fund managers this is not an issue, mainly due to the diversification of the portfolio. As many VC investors also would argue, the return is dependant on the VC company.

”Buyout funds, which are the most popular form of alternative investment, do not vary in terms of returns whether they are in the top quartile or not. But for the top quartile within VC it can make a huge difference. One can say that VC is a very expensive asset class when it goes bad, and very cheap when it goes well,” Pärson says.

VC is a very expensive asset class when it goes bad, and very cheap when it goes well

Sweden is leading the race when it comes to the proportion of pension funds invested in VC, and may draw even further away from other European countries. In 2018 a new directive was issued in Sweden, which lets private pension schemes increase their share of alternative investments from 5% to 40% of the funds.

For the VC companies in Sweden, the new rules create happy hour all year round.

“10 years ago, the usual response from pension funds was that they had already filled their quota on alternative investments. Now we see much higher volumes of incoming calls, and the new directive makes a huge difference”, Pärson says.