French youth want to set money aside for travel and buy a flat, as well as invest more, but 65% feel the banking products on offer aren’t helping them get there.

The survey of 18- to 35-year-olds released on Monday by OpinionWay and fintech Moka suggests traditional banks aren't catering to millennials' financial demands.

At the same time, 48% of respondents said they have trouble setting money aside each month, and half saying they’ve never invested money before.

The results are just one study, but it speaks to the opportunity for new financial companies to disrupt high-street banks.

Already in France, there are dozens of financial technology companies attempting to win over a younger audience, including Kard and Lydia.

Meanwhile, user-friendly investment apps are also booming in Europe, with Germany's Trade Republic recently closing a €62m fundraise and Holland's Bux hitting 300,000; making it the largest neobroker in Europe.

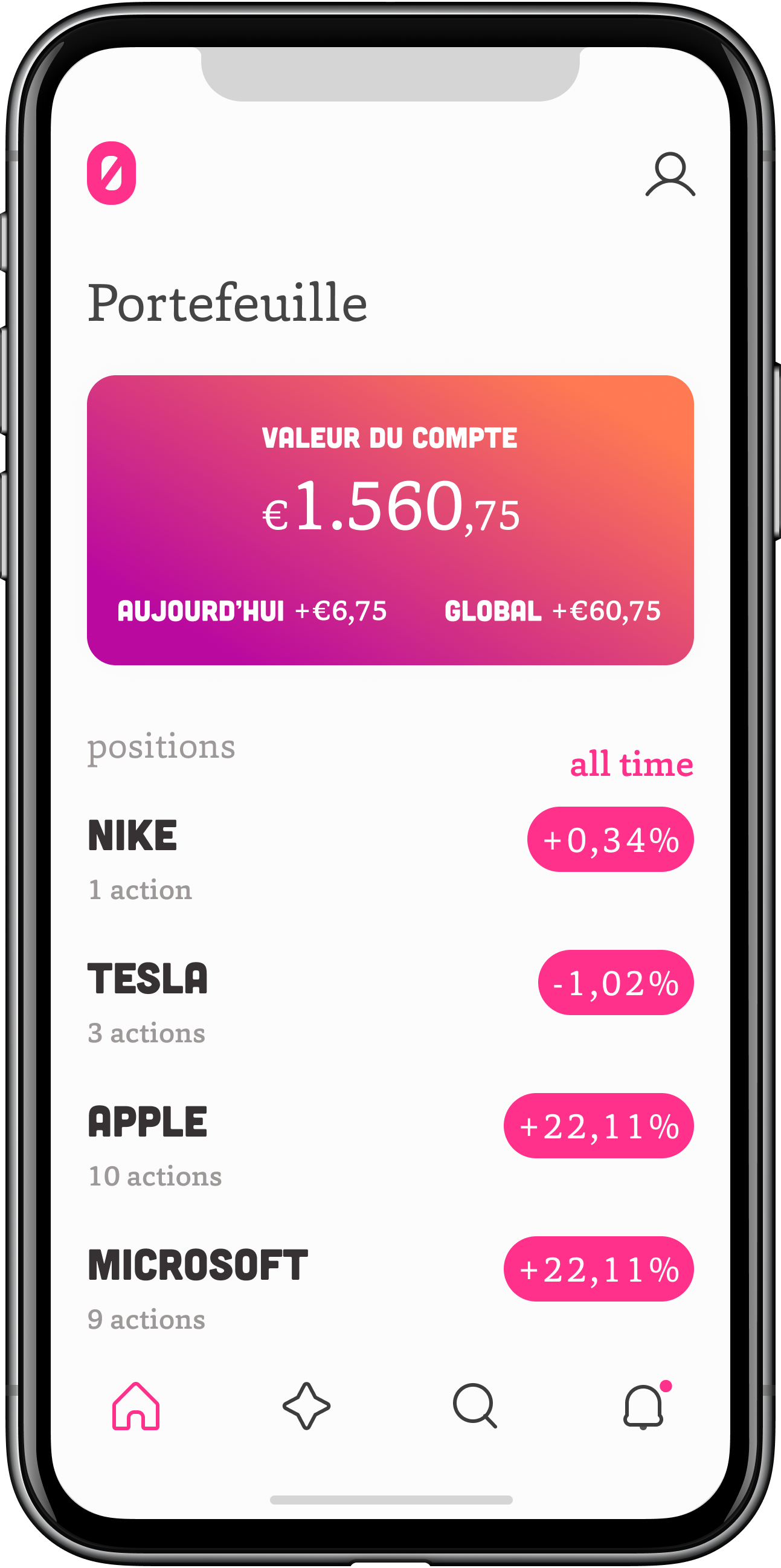

There is a range of different models emerging in the wealth tech space as well. Efforts to woo younger Europeans into investing span from no-fee stock-trading platforms, to crypto trading (as seen in the Revolut premium app), to more simple 'basket' investing, seen in apps like Plum, Dreams and Tickr.

Investors have been pouring money into the sector, seeing an opportunity in the sluggish response of well-established banks and seeming inability to create new youth-focused brands themselves.

“Traditional French banks never transformed their savings and investment services,” says Maxime Le Maitre, who works for Canada's Moka, the fintech which commissioned the survey. Formerly known as Mylo, the Canadian startup is renaming itself Moka as it prepares to launch its investment app into the French market, with Le Maitre managing expansion into a new country.

OpinionWay conducted the survey online in May with 1,003 respondents in the country, within the 18 to 35 years old age group.

Moka

Moka’s pitch is that it can show young adults that saving and investing can be simple, effortless and fit any budget; targeting a demographic they say has been ignored by traditional banks.

Moka allows users to start investing with 1€ and offers investment portfolios built with criteria like social responsibility in mind.

Its app plugs into existing bank accounts to round up amounts spent for purchases and lets users invest the change into pre-set diversified stock market portfolios. The app is free the first month and costs a fixed subscription of a few euros each month after that.

In France, homegrown fintechs Birdycent and Yeeld offer similar apps based on putting money aside by rounding up amounts spent. Many of those services are free — and several have been around for many years. Well-established traditional banks like LCL have also launched a similar service called “Option System'Épargne”, which debuted in 2008.

However, none have so far had a disruptive effect on the French investing market nor on young Frenchies’ habits.

Moka is now betting that the coronavirus crisis will act as an accelerator.

65% of the OpinionWay poll’s respondents say they see the Covid-19 crisis as an opportunity to set money aside and invest to help face a more uncertain future, while half of those polled say they thought about making financial investments during lockdown.

Moka may soon face competition, as Holland's Bux has announced today it is expanding its stock-trading offering in France. Nonetheless, the two have slightly different audiences, as Moka targets beginner traders who prefer 'basket' investing, while Bux allows more experimental users to buy pure stocks or cryptocurrencies.