Covid-19 has created a huge opportunity for fintechs, but there’s one major obstacle — trust.

Specifically, there are four key areas of concern which appear to drive distrust of fintechs; data privacy, fear of the unknown, limited regulation and sector scandals.

Two of these 'trust gaps', I believe, are becoming less potent over time, but the other two are actually fuelling people’s aversion to fintechs — and could prevent the sector from riding the new wave of digital acceleration.

The following draws on extensive research crafted over the last two decades; surveying over 33,000 individuals annually for Edelman's Trust Barometer.

You want my data?

Data privacy and how data is used have been a growing source of concern for years. This has proven to be a major hurdle for the open banking reforms in the UK, for instance, with consumers reluctant to share personal data with fintech apps, even if it meant accessing better or more competitive products and services.

However, the advent of ‘track and trace’ apps to control the virus could well be the catalyst for new norms around data sharing and help address this particular trust pain point for fintech apps.

The latest research shows that 62% of people are willing to give up more of their personal data in order to help track and contain the virus. In other words, people are becoming more comfortable with the idea that their data can be used responsibly and for good — and that data sharing is simply becoming a part of life.

Fear of the unknown

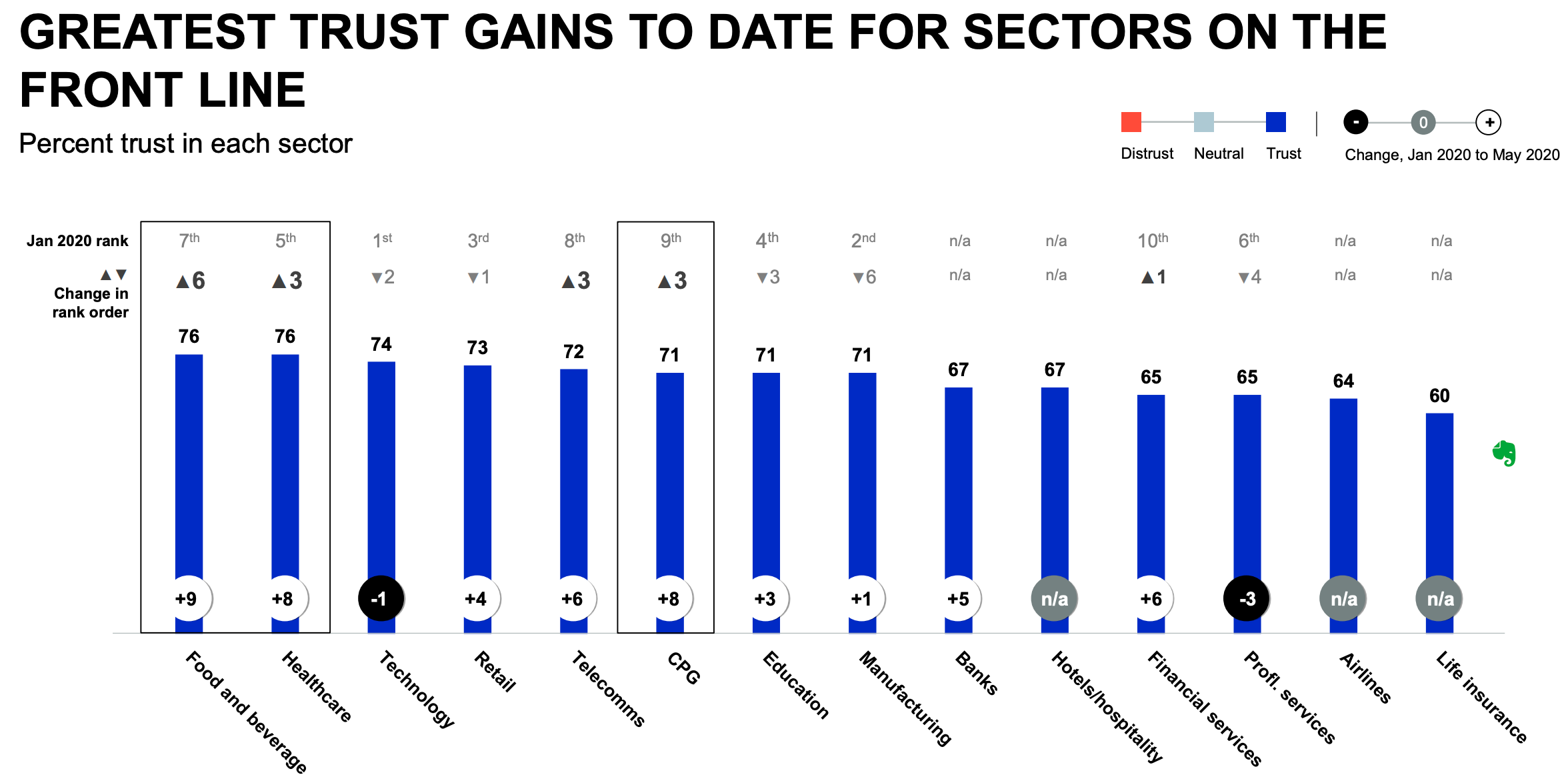

Another issue that hinders fintechs is fear of the unknown, which means people still trust major, established financial services companies far more.

64% of people on average say they trust banks, insurers and wealth managers whilst only 47% say the same for peer-to-peer and digital payments companies, 48% for blockchain and crypto companies and 49% for digital wealth and robo-advisory firms. In fact, trust in these fintech sub-sectors is even weaker amongst the very demographics that many are purportedly designed to help; those in lower socio-economic groups.

Nonetheless, over time, this gap should shrink organically and we are already seeing year-on-year improvements in trust levels across all fintech sub-sectors, as familiarity gradually builds.

In particular, companies which are consistently visible, front-of-mind and credible voices on relevant issues will bridge this trust gap quickest.

Moving too fast

More broadly, people also believe that technology is advancing faster than they're able to get comfortable with it.

61% of people told us this year that “the pace of technology is too fast”. The same number said they thought the UK government does not understand emerging technology enough to regulate it effectively. 66% stated that they worry that technology makes it impossible to know whether what they are seeing and hearing is real or not.

If technology is increasingly seen as a sinister influence, that could override any improvement in familiarity with the leading fintech brands, and hence worsen the trust gap overall.

Most fintechs are predicated on the notion that they are a force for good — but the tide of opinion is turning against technology companies.

Indeed, most fintechs are predicated on the notion that they are a force for good — simplifying and democratising a creaking, inequitable system — but the tide of opinion is turning against technology companies, fuelled by growing concerns over our ability to keep them in check. The challenge will be to walk the tightrope between moving admin, process and inefficiencies out of customers’ minds but not entirely out of their sight.

A degree of so-called “over-transparency” may be needed to ensure people feel in control of the financial technology they use rather than the other way round.

Scrutiny and scandals

As any sector gets more prominent, so too does the level of scrutiny applied to it and the societal and business impact of scandals and failures pertaining to it. US investment platform Robinhood’s recent backlash following the suicide of one of its customers received widespread media coverage. The spectacular collapse of German fintech Wirecard has been the largest corporate news story of the year and is about to be turned into a documentary by the German broadcaster RTL.

As any sector gets more prominent, so too does the level of scrutiny applied to it and the societal and business impact of scandals and failures pertaining to it.

In the year following a high-profile damaging event involving a company or individual, our data shows that trust in an entire sector can suffer. The automotive industry saw a major decline in trust between 2015 and 2016 thanks to the ripple effect from the emissions scandal; this year, big tech’s failure to clamp down on racism and misinformation precipitated a similar dip. The looming shadow of Wirecard means the fintech sector, as a whole, will need to work harder than ever to demonstrate both its social corporate and its corporate governance credentials.

Fintech is at a trust crossroads. There are many reasons to believe that the sector should be the standard bearer for business as we move into a post-Covid era and some areas of historical distrust in fintechs are now receding. However, widespread adoption will ultimately depend on fintechs’ collective ability to bridge the trust gap between themselves and the larger names in finance.