Two years ago, the British Business Bank — the UK government’s development bank — set up a new subsidiary, British Patient Capital (BPC), with £2.5bn to invest to “enable long-term investment in innovative firms led by ambitious entrepreneurs”.

It has now made over £1bn worth of commitments — and seen third-party investors commit £4.8bn alongside it. It’s the UK’s largest domestic investor, and is even (unexpectedly) turning a profit (of £4m before tax) at this point in its 10-year lifespan.

As of March this year, it had backed 32 fund managers, across 42 funds — including Hoxton Ventures, Kindred and Connect Ventures — and had over 500 startups in the underlying portfolio. Since then, it has made six new fund commitments.

It’s also recently started making direct investments into later-stage companies — such as data analysis startup Quantexa and banking software startup Thought Machine — alongside the fund managers it has backed.

And that’s not the only coinvestment the BBB has been dabbling in. In response to the coronavirus pandemic, it also launched the Future Fund, a £500m+ pot of capital to back UK startups alongside other venture capital investors. As of October 20, the Future Fund had approved £770.8m worth of convertible loans for 745 companies.

Sifted sat down with the interim CEO of BPC, Judith Hartley, to discuss its plans for the future — and why the only other startup ecosystem she’s keeping an eye on is the US.

Is the primary role of BPC to unlock other third-party investment — that £4.8bn to date?

It’s a fundamental part of our role. The idea has always been to attract third-party investors to invest alongside, so [our capital] is leveraged up and becomes more and more. We want to create a track record in this area, so it becomes more attractive to private sector investors.

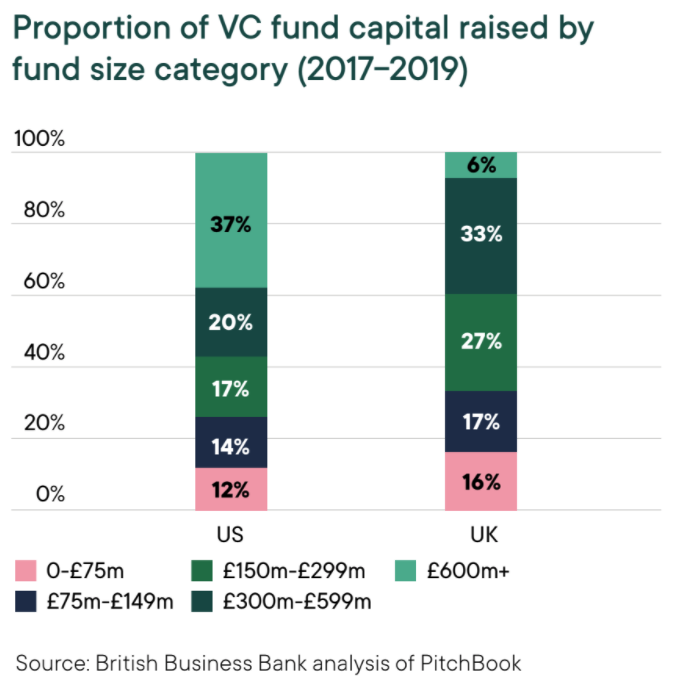

As we look to the future, with £1.5bn left to deploy, we’ve started to focus on the venture growth side of the market. When we look at Series B+ and compare that to the US, the round sizes are half the size. We need to put extra firepower into this area to help the UK market catch up.

The main thing is to make sure that these scaleups have got money available to scale up — that they know where to go, and that it is there.

And is it mostly the US that you look to, rather than Europe?

We look at both. But we’re strong in the UK compared to Europe, so we really want to prevent those high-potential fast-growth companies upping sticks and moving to the States, or getting bought out. We’re trying to even things up so the UK can catch up — the vision is that any innovative company that has the potential can grow here.

We really want to prevent those high-potential fast-growth companies upping sticks and moving to the States.

How does BPC choose which funds to invest in?

We’re principally looking for fund managers who are best in class, who meet the investment criteria that we set and will be there for the long term. We don’t deliberately pick sectors, but we are interested in fund managers’ investment strategy and what that would give us in terms of underlying companies.

Across our existing portfolio, 15% are in life sciences — and there are further life sciences opportunities coming through in our pipeline — so we’ve appointed a life sciences director to give us more skills and capability in that regard.

BPC has also started coinvesting alongside funds in startups. Why?

To make sure this company has that financial firepower, to make sure they can keep on growing. It’s always been part of our strategy; we started to do coinvestments in this financial year, and going forwards we’re looking to ramp that up further. We’ve done two so far, we may do another one to two this financial year. It depends on opportunities. We’ll probably do four to six per year.

Yale recently said that it’s going to start measuring the firms it invests in on their progress towards having more diverse teams. Would the BPC consider doing something similar?

It’s something we’re really interested in. We follow ILPA assessment guidelines and as part of our investment diligence into companies and funds, we look at diversity and inclusion. For fund managers, we look at what policies they have for their own organisation, and how they approach that with investee companies.

At BPC ourselves, three of our four board members are women and we have a very diverse team. So yes, it’s something we want to champion and something we actively check and diligence as part of our reviews.

Do you think having stricter diversity criteria would send a strong message to the market and have an even greater impact?

Yes it would — but it would limit potential opportunities that come in, so it would have to be a balance overall.

You’ll have seen the latest data from the BBB last week [from the Future Fund]. In terms of diversity and inclusion, it’s something we’re focused on at the BBB as well as BPC.

On the Future Fund, all I can say is that it’s a temporary programme, set up for a particular reason. At BPC, by contrast, we’re here for the long term, we’ll be here after the crisis. We’re not a one-off.

One final crazy idea — which one of your fund managers, who I won’t name, suggested to me. Do you think BPC should limit the salaries fund managers can pay themselves (with tax-payer money), seeing as if they do a good job they should make a tidy return from their carry anyway?

We invest on a pari passu basis with the private sector, and we match those terms. So we wouldn’t want to be putting in place terms that are contrary to what the private sector would accept or would put off private sector investment. It would be self-defeatist.

When Covid first hit, it wasn’t clear what would happen to the VC fundraising landscape. What have you seen pan out from your side?

It’s quietened. The pipeline is still pretty full, but it’s slower to pass through — we’re still looking to invest, but the issue is that third-party investors are cautious, given what’s going on in the market. Other institutional investors have slowed down.

In terms of the portfolio, it’s been broadly resilient to any negative impact — and quite buoyant in some areas.

And what about Brexit: a lot of your equivalents in Europe seem to be rubbing their hands in anticipation… Do you think it will actually have as much impact on the UK tech ecosystem as they think?

We need to be there and have lots of firepower available so we can step in where the European Investment Fund may have previously been involved, and won’t be anymore. We will fill gaps as far as we possibly can. We have £1.5bn to deploy still — so they may be rubbing their hands, but we’re alright.

*This conversation has been lightly edited for length and clarity.